中国のグリーン・スチール移行を可能にする: 設備投資の展開、電力網の脱炭素化、そして補助金支援

Key Takeaways

Declining CAPEX is narrowing the cost gap of green steel

Technological learning and China’s strong domestic manufacturing base are driving down capital costs for renewable energy, storage, and electrolysers, making H2-DRI-EAF steelmaking increasingly cost-competitive. Continued investment in R&D and cost optimisation—particularly in iron reduction technologies like shaft furnaces—could further lower CAPEX and help China establish a stronger technological foothold in low-carbon steel production.

Grid decarbonisation is pivotal to green steel viability

Regional differences in electricity carbon intensity and pricing significantly affect the emissions and cost profile of hydrogen-based steel. Provinces with cleaner, lower-cost electricity can achieve green premiums below 10%, enhancing commercial viability. To enable this transition, both provincial and central governments must prioritise grid integration and implement clear, ambitious decarbonisation plans for China’s power sector.

Well-designed subsidies can unlock large-scale deployment

Among the available policy tools, CAPEX subsidies are the most cost-effective for lowering the Levelised Cost of Steel (LCOS). Policymakers should focus on delivering the most efficient forms of support, rather than relying heavily on less effective market-based instruments like low-cost financing, which are better handled by financial markets. Strategic, well-targeted subsidies remain essential for closing the cost gap and enabling the large-scale deployment of green steel.

Introduction

As the world’s largest steel producer, China faces a monumental challenge in its quest to reach carbon neutrality by 2060. The steel sector, a major contributor to national and global greenhouse gas emissions, must undergo profound transformation. One of the most promising pathways is the adoption of green hydrogen-based direct reduced iron combined with electric arc furnaces (H2-DRI-EAF)—a technology that holds the potential to produce near-zero-carbon “green steel” and fundamentally reshape the industry.

Yet, this low-carbon process currently comes at a steep price. Green steel via H2-DRI-EAF remains significantly more expensive than conventional steel made in coal-based blast furnaces. Market demand for such products is still nascent, with few signals of buyers’ willingness to absorb “green premiums” of low carbon steel beyond a small number of automaker-steel company MOU’s. Moreover, the true cost of scaling this technology remains uncertain, especially given the limited number of H2-DRI-EAF facilities currently operating in China.

This presents a pressing economic dilemma: What would it cost China to scale up green steel production, and how can these costs be reconciled with the realities of a price-sensitive, globally competitive market?

The H2-DRI-EAF Process: A Paradigm Shift in Steelmaking

Conventional steel production through the blast furnace-basic oxygen furnace (BF-BOF) pathway is highly carbon-intensive, averaging 2.1tCO2 per tonne of steel in China, relying on coal and coke to reduce iron ore into molten iron.1 In contrast, the hydrogen-based direct reduced iron-electric arc furnace (H2-DRI-EAF) process presents a less carbon intensive, near zero emission alternative:

Direct Reduced Iron (DRI): Rather than using a blast furnace, iron ore is reduced in a DRI reactor using a hydrogen-rich reducing gas. This reaction removes oxygen from the ore, producing a solid metallic iron known as direct reduced iron or “sponge iron.”

Green Hydrogen (H2): In this process, hydrogen is produced via electrolysis—a method that splits water into hydrogen and oxygen. When powered by renewable energy sources such as solar and wind, this process yields “green hydrogen,” enabling a nearly carbon-free reduction of iron ore.

Electric Arc Furnace (EAF): The DRI, along with scrap steel, is melted in an electric arc furnace to produce liquid steel. When powered by renewable electricity, the EAF process further reduces the overall carbon footprint.

This innovative pathway can cut CO₂ emissions by over 95% compared to the BF-BOF method, positioning it as a cornerstone of global steel sector decarbonisation strategies. In this analysis, we follow the International Energy Agency (IEA) standard, defining “near-zero emission steel” as steel with lifecycle emissions below 0.4 tCO₂ per tonne of output with no scrap.2

Provincial H2-DRI-EAF modeling presents varying results

This analysis uses a techno-economic optimisation model to evaluate the cost of producing green steel via H2-DRI-EAF across China’s provinces in the year 2030. The model operates at provincial spatial resolution, allowing us to capture local variations in renewable energy availability and electricity grid emissions—both of which critically influence the feasibility and cost of green steel production.

The model minimises the levelised cost of steel (LCOS) by optimising the mix and capacity of:

- On-site solar and wind generation

- Battery storage and hydrogen storage

- Grid electricity purchases

We incorporate:

- Provincial renewable resource potential, based on hourly solar and wind capacity factors

- Provincial grid emission factors, to reflect regional electricity decarbonisation levels

- Projected 2030 capital and operating costs for renewables, electrolysers, and DRI-EAF facilities, accounting for expected cost reductions through technological learning

Regional Cost Landscape

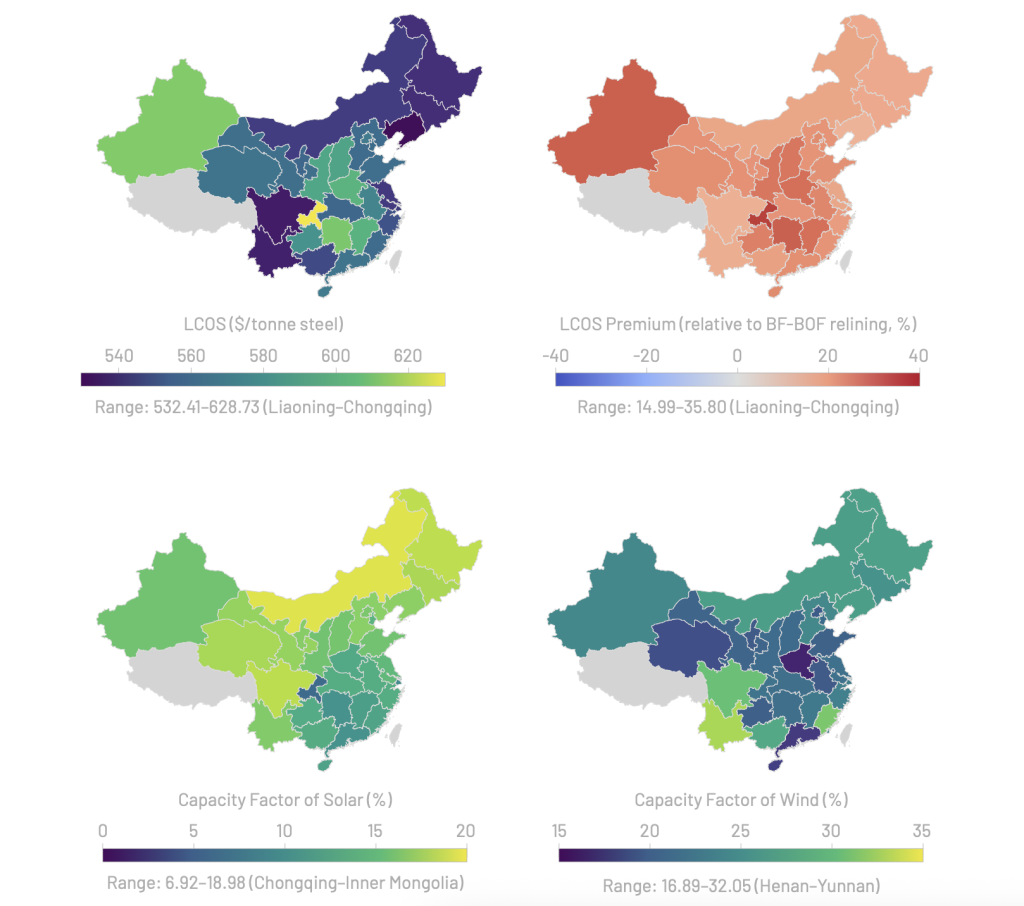

The economic feasibility of H2-DRI-EAF in China is strongly influenced by geographic variation in renewable resource potential. As shown in Figures 1&2:

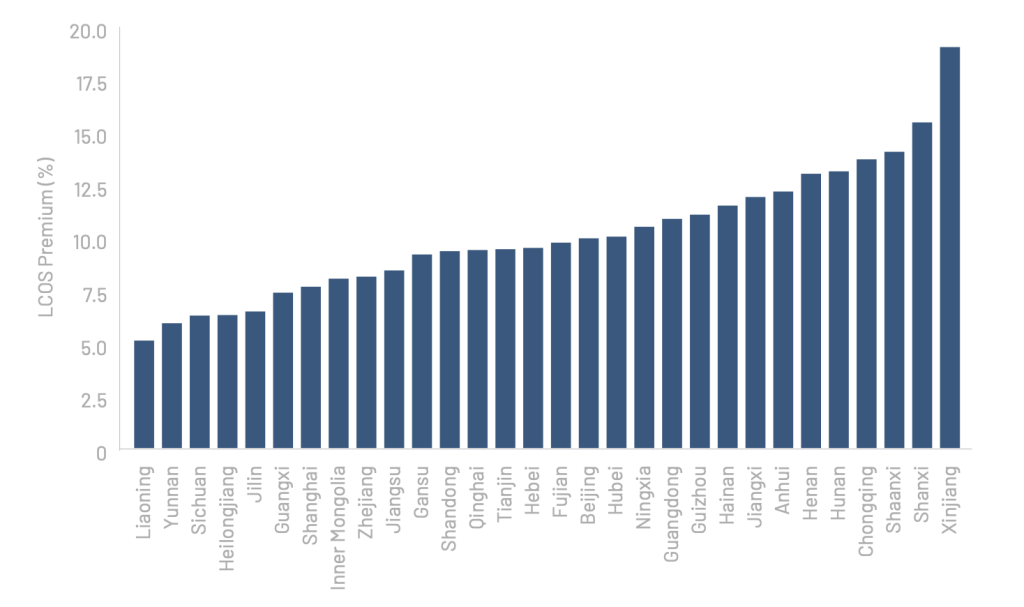

- Driven by differences in renewable resources and grid emission factor in different provinces, the Levelised Cost of Steel (LCOS) ranges from approximately $530 to $630 per tonne, with Liaoning emerging as the most cost-effective province. This reflects a 14–35% premium over the LCOS of relining BF-BOF, which is estimated at approximately $460 per tonne for 2030.

- LCOS is highly sensitive to local renewable resource availability, especially solar power. Therefore, northern provinces tend to exhibit lower LCOH due to higher solar capacity factors.

Importantly, several of China’s major steel-producing provinces show relatively favourable economics for H2-DRI-EAF:

- Liaoning, China’s fourth-largest steelmaking province3, boasts the lowest LCOS across all regions. Considering its strong industrial base, skilled labour pool, logistical infrastructure, and robust grid connections, Liaoning presents a compelling opportunity for early H2-DRI-EAF pilots or retrofitting of existing BF-BOF capacity.

- Jiangsu, Hebei, and Shandong, also major steel-producing provinces, rank 6th, 13th, and 17th respectively in LCOS. While their LCOS is higher than some provinces, these regions still represent promising candidates for H2-DRI-EAF deployment. With strong grid infrastructure and industrial capacity, they can benefit from integration with renewable electricity and hydrogen transported from nearby lower-cost provinces to achieve cost-effective green steel production.

- Provinces such as Sichuan, Yuan, Jilin, and Heilongjiang, though not current steel production hubs, offer low LCOSs due to outstanding solar and/or wind resources. These areas are well-suited for greenfield H2-DRI-EAF development for capacity swap from provinces with high LCOH (e.g., Henan, Jiangxi), or as strategic green hydrogen production hubs supplying downstream industrial centers.

Figure 1. Provincial LCOS of H2-DRI-EAF, Green Steel Premium, and Solar/Wind Capacity Factors

Map by Free Vector Maps

Source: TA analysis

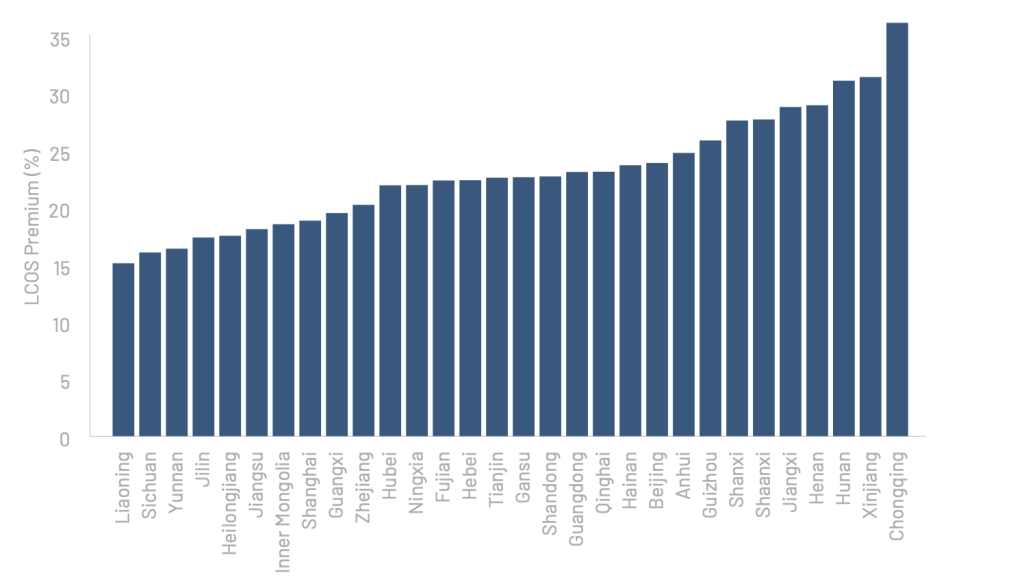

Figure 2. Average Provincial Lowest Cost Green Steel Premium (%) Relative to average BF-BOF Cost

Source: TA analysis

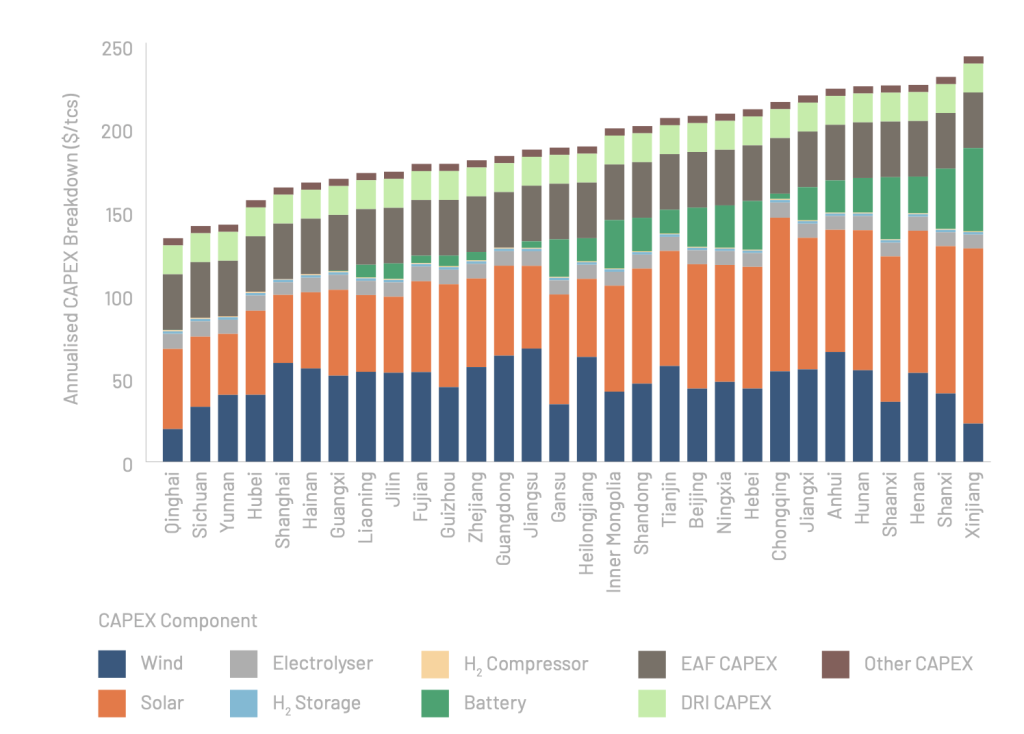

Drivers of Capex - Overview

The cost structure of H2-DRI-EAF systems in China is shaped by both global technology dynamics and China-specific cost advantages. As shown in Figure 3, the CAPEX is primarily driven by: onsite solar PV (32%), onsite wind turbines (26%), Electric Arc Furnace (EAF) units (18%), and DRI shaft reactors (9%).4

This breakdown reveals three key drivers of capital investment:

1.Renewable Energy Supply (Wind + Solar)

Reliable and affordable renewable electricity is fundamental to green steel economics. Hydrogen production in particular requires high electricity input: for each tonne of H2-DRI-EAF steel, DRI-EAF consumes 833 kWh, and hydrogen production requires 2,971 kWh. As a result, onsite renewable generation accounts for nearly 60% of total CAPEX. In two-thirds of provinces, solar PV dominates due to its high power density, although the specific mix depends on regional resource profiles.

The intermittency of renewables—particularly solar—necessitates a hybrid configuration. Integrating wind, solar, and energy storage systems (battery and hydrogen) ensures high-utilisation of hydrogen electrolysers and stable supply for H2-DRI-EAF operations. As the world’s largest manufacturer of wind turbines, solar PV panels, and lithium-ion batteries, China benefits from economies of scale and a mature supply chain, enabling cost-effective deployment of renewable infrastructure.

In this study, pressurised hydrogen storage is capped at 20 kg H₂/tonne steel due to safety constraints. Battery and hydrogen storage systems play complementary roles in stabilising hydrogen supply, and their role is expected to grow with continued technological and cost improvements.

Importantly, total CAPEX does not directly correlate with LCOS (Figure 3), as some provinces with weaker renewable resources may compensate through greater use of grid electricity, depending on local grid emissions and renewable availability.5 In our analysis, we assume zero-cost land access and grid connection—an assumption that may be reasonable given that land provision and infrastructure support are commonly used by the Chinese government as policy incentives to promote industrial decarbonisation and renewable investment.6Grid connections are especially important, as renewable energy projects that support green steel production will require large land areas. This can result in considerable distances between the energy generation sites and the hydrogen-based steel plants, making transmission infrastructure essential.

2. Steelmaking Equipment: DRI Shaft Reactors and EAF

The DRI shaft reactor is a critical component in green steel production, but remains expensive due to a global supplier duopoly between Midrex (USA) and Tenova/Danieli (Italy). Protected by intellectual property and technical complexity, this limited competition keeps prices high. However, recent China-Iran cooperation on technology transfer could open opportunities for domestic production and reduce costs.

EAFs, by contrast, are well-established and widely used in both scrap- and DRI-based production. Their costs scale predictably with capacity and the technology is flexible. Nonetheless, producing high-grade or specialty steels may require more advanced feedstock strategies and process controls. Whilst China has considerable experience in manufacturing EAFs for scrap use, there has not been demand for EAFs producing steel for high grade applications. Currently this EAF technology is dominated by Western companies such as Danieli and Prime Metals.

3.Hydrogen Production System

Hydrogen production—including electrolyser cells, Balance of Plant (BoP), and installation (EPC) costs—accounts for around 6% of total CAPEX. While this is a major cost driver globally, China maintains a significant competitive edge. Domestic alkaline electrolysers are priced as low as $271/kW, nearly one-fourth the cost of systems in Europe or the U.S., thanks to mature supply chains and large-scale manufacturing.7 As a result, hydrogen production contributes only modestly to CAPEX in China, enhancing the viability of the H2-DRI-EAF pathway.

In summary, China’s comparative advantage in renewable energy infrastructure provides a solid foundation for large-scale green steel deployment. To further reduce costs and accelerate adoption, domestic innovation in DRI shaft production and enhanced EAF capabilities will be essential.

Figure 3 Breakdown of Annualised CAPEX of H2-DRI-EAF

Source: TA analysis

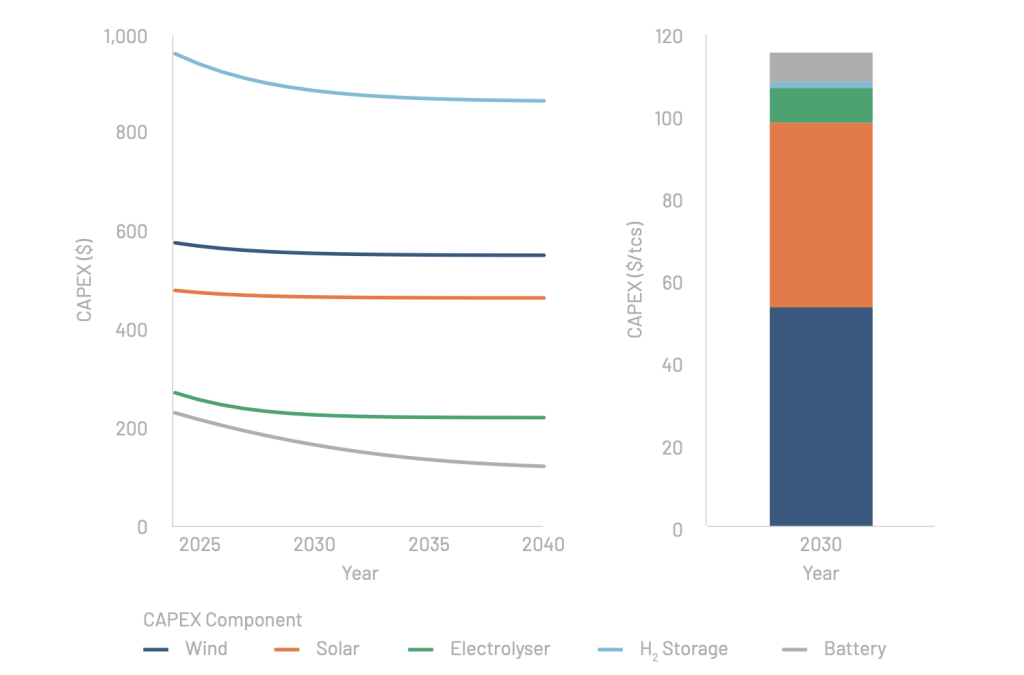

How Technology Advancements Shape CAPEX

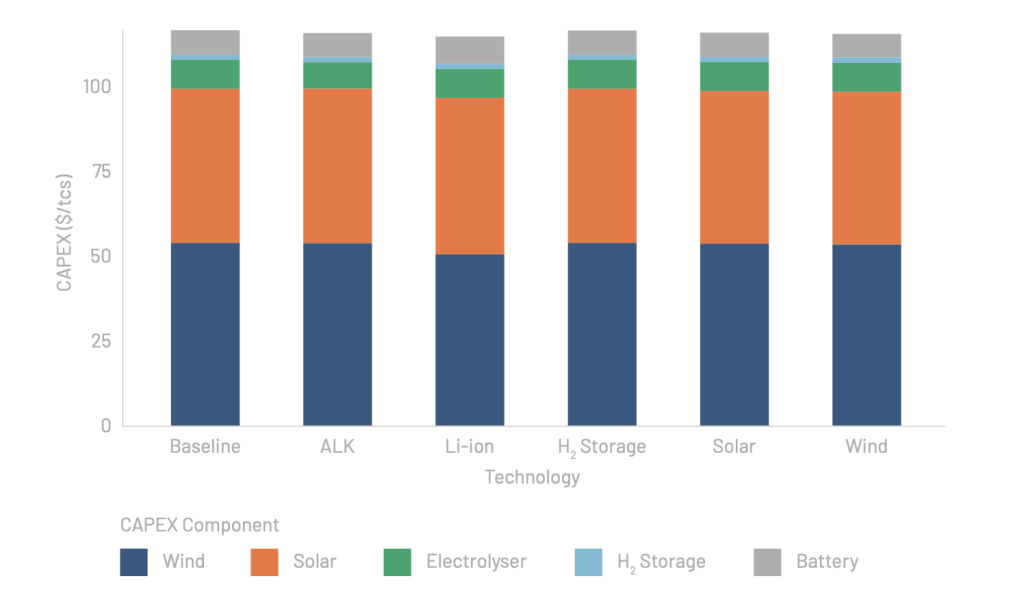

Figure 4 illustrates the learning curves associated with five key technologies (i.e., wind turbine, solar PV, alkaline electrolyser, hydrogen storage, and li-ion battery) used in H2-DRI-EAF systems. The projections use learning rates and technology maturity levels as of 2024 to estimate future CAPEX.8 Technologies such as battery and hydrogen storage display steeper cost declines due to their relatively early-stage maturity compared to more established wind and solar technologies. These cost reductions translate into significantly lower capital investment requirements in future projects, as shown in the right panel of Figure 4.

To assess the effect of accelerated innovation, we introduce a “learning rate boost” scenario (Figure 5) , where each technology improves 50% faster than in the baseline (i.e., current learning rate × 1.5). This scenario reflects the potential impact of increased R&D investment, improved manufacturing, or targeted policy support.As expected, faster learning leads to lower CAPEX, though the impact varies by technology. Battery cost reductions result in the largest decrease in system CAPEX and enable more battery deployment in the optimised system. The results emphasise that both the learning rate of each component and its contribution to LCOS determine the system-level cost impact.

These findings suggest that accelerated technological progress can make green steel more affordable, particularly by reducing upfront investment requirements. They also highlight China’s strategic advantage: with large-scale domestic production of solar panels, wind turbines, batteries, and cost-effective alkaline electrolysers, China is well positioned to lead global efforts in scaling H2-DRI-EAF deployment and reducing its costs through sustained innovation.9

Figure 4. CAPEX decreases as technology advancement (right panel: Liaoning Case Study)

Source: TA analysis

Figure 5. Impact of Accelerated Technological Learning on CAPEX and System Configuration (Learning Rate Boost Scenario, current learning rate x 1.5, Liaoning)

Source: TA analysis

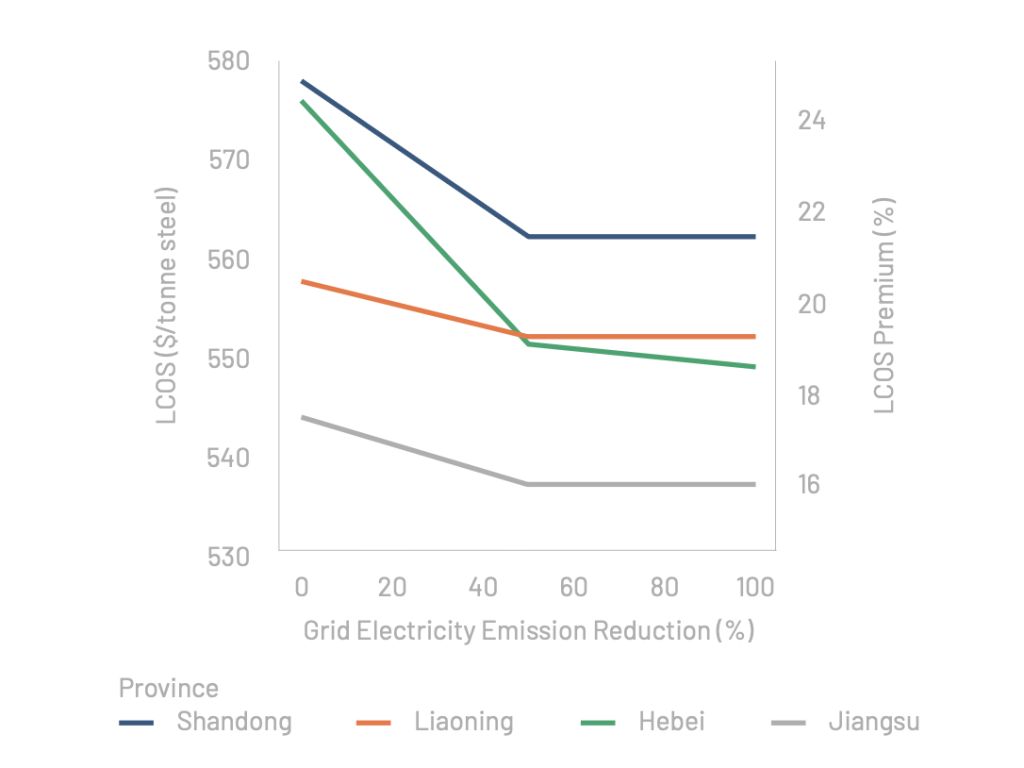

Grid Emission Factor and LCOS

Beyond renewable resource quality, provincial grid emission factors play a significant role in shaping green steel feasibility. Under current conditions, grid electricity accounts for more than 85% of total CO₂ emissions in an H2-DRI-EAF system—constrained by the 0.4 tCO₂/tonne steel threshold used to define near-zero emission steel. This emissions constraint forces steel producers to invest heavily in on-site renewable generation and energy storage to limit reliance on the grid, particularly during periods when intermittent renewables fall short.

As China decarbonises its power system, the grid emission factor will decline. This transition could ease the burden on steelmakers by allowing greater flexibility to use grid electricity. As shown in Figure 6, halving the current grid emission factor results in a $7–18 per tonne reduction in LCOS across provinces. However, further reductions in grid emissions (e.g., assuming a fully decarbonised grid) produce only marginal cost savings. This is because on-site renewable generation is already more cost-effective than grid electricity in most provinces. In such scenarios, grid electricity primarily serves to supplement renewables during shortfalls, rather than replacing on-site capacity altogether.

These findings highlight the interconnectedness of power system decarbonisation and industrial decarbonisation. Accelerating the clean power transition can reduce the cost and increase the flexibility of green steel production—offering critical support to decarbonising hard-to-abate sectors like steel.

Figure 6. LCOS Reduction with Declining Grid Emission Factor (Relative to Current Levels)

Source: TA analysis

Role of Subsidies in Lowering LCOS

China’s steel sector is central to the country’s industrial output and energy consumption, contributing over 15% of national CO₂ emissions. As part of its broader climate goals—including carbon peaking before 2030 and carbon neutrality by 2060—China has begun signaling strong policy interest in decarbonising hard-to-abate sectors like steel. Policy tools such as green bonds, innovation grants, low-carbon pilot programs, and electricity pricing reforms have already emerged in related sectors, but targeted support for green steel remains nascent. In this context, financial incentives—whether through direct capital support, electricity cost relief, or carbon performance rewards—could play a transformative role in scaling up H2-DRI-EAF deployment and closing the cost gap with conventional steel.

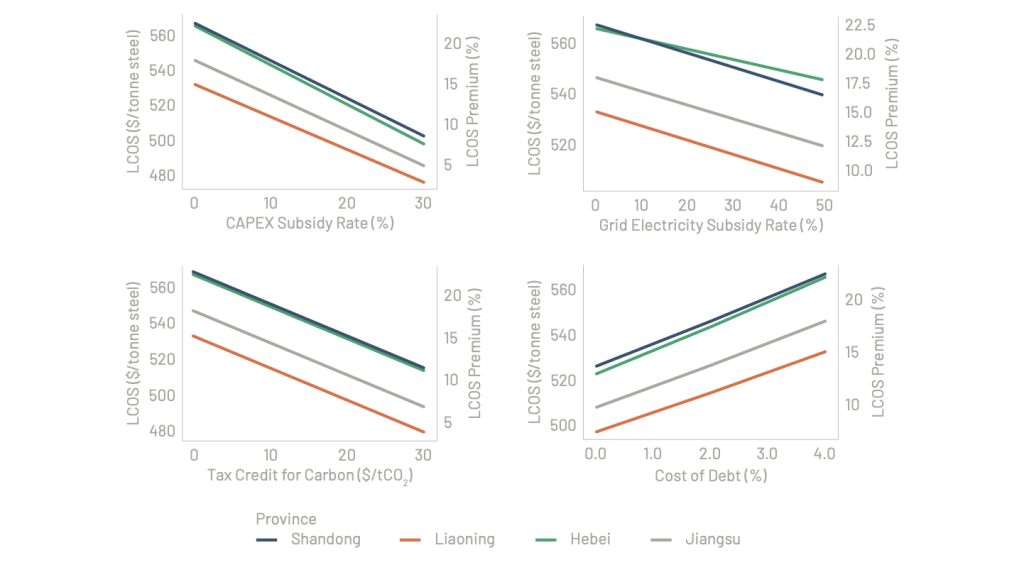

Subsidies and supportive financing mechanisms can significantly influence the competitiveness of green steel. In this analysis, we tested the impact of these subsidy types:

- CAPEX subsidies (as a ratio of total capital expenditures): One-time government contributions that reduce initial investment costs for building renewable or steelmaking infrastructure. For example, under China’s national guidance for energy-saving and carbon-reduction projects in key industries—including steel—central and local governments may offer funding of up to 20% of total project investment.10

- Subsidised electricity prices (as a fraction of the base grid electricity price of $0.086/kWh): Discounted electricity tariffs offered to industrial users to lower operating costs when using grid power. While China is moving to eliminate broad-based electricity discounts for energy-intensive industries, it is also promoting a tiered pricing system that links electricity rates to energy efficiency and environmental performance. This shift opens the door for targeted, merit-based subsidies that could benefit green steel producers.11

- Carbon reduction tax credits (in $/tCO₂ reduced, benchmarked against BF-BOF emissions of 2.1339 tCO₂/tcs): Financial incentives provided per tonne of CO₂ avoided, rewarding emission reductions and improving project economics. In China, policy directives such as the Environmental Protection Tax Law give tax incentives to steel enterprises that meet ultra-low emission conditions. For example, enterprises that adopt ultra-low emission technologies are eligible for preferential tax treatment, and investments in dedicated environmental protection equipment can qualify for corporate income tax deductions.10

- Concessionary finance (the interest rate applied under a fixed debt ratio of 70%): Loans offered at below-market interest rates or with favorable repayment terms to lower the overall cost of capital. Interest rate incentives have been widely adopted in China as part of green finance initiatives, particularly through instruments like green credit and preferential loans under national carbon reduction policies.12

As shown in Figure 7, all four types of subsidies reduce LCOS approximately linearly. In Liaoning, where conditions are already favourable, a 10% green premium (i.e., achieving $506/tonne LCOS versus $460/tonne BF-BOF cost) can be achieved through multiple pathways:

- A 10% CAPEX subsidy;

- A 45% electricity price subsidy under the current grid emission factor;

- A $10/tCO₂ carbon tax credit;

- An interest rate of 1% under a 70% debt ratio.

For provinces with higher LCOS, the required subsidy level or payment would need to be higher and scale accordingly.

Figure 7. LCOS Reduction with Different Subsidies in Liaoning, Shandong, Hebei, and Jiangsu

Source: TA analysis

Source: TA analysis

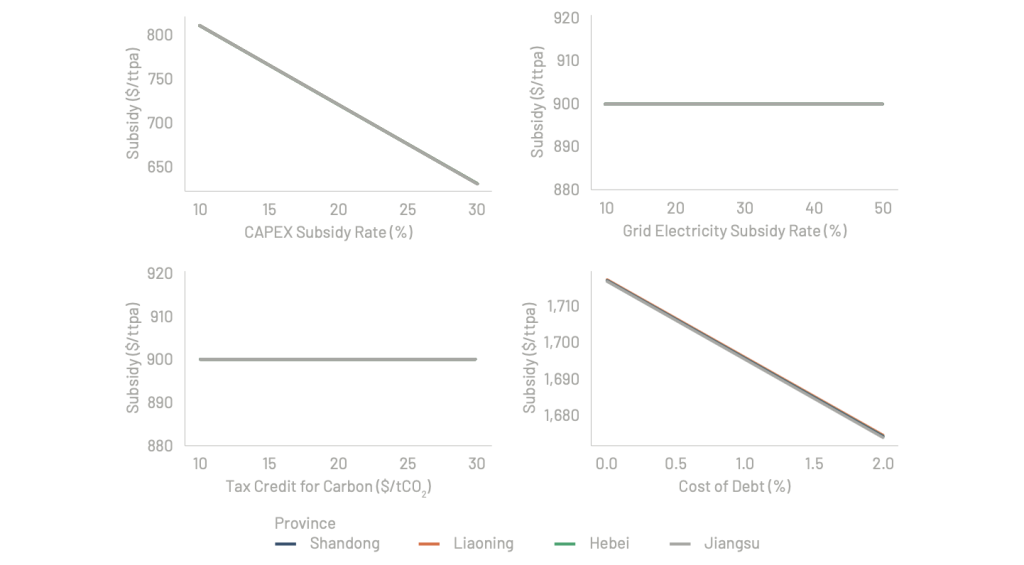

However, each type of subsidy imposes a different fiscal burden. To assess cost-effectiveness, Figure 8 shows how much subsidy is needed to reduce LCOS by $1 per tonne for each 1,000 tonnes per annum (ttpa) of steel production capacity:

- Concessionary finance is the least efficient, costing up to $1,700/ttpa per $1 LCOS reduction due to compounding interest effects.

- CAPEX subsidies are the most efficient, and their cost-effectiveness improves at higher subsidy levels due to the compounding benefit of reduced financing needs—larger upfront support lowers not only capital costs but also interest payments over time.

- Electricity price subsidies and carbon tax credits, both operational subsidies, exhibit constant effectiveness—roughly $900/ttpa per $1 LCOS reduction.

It’s important to note that while operational subsidies scale with production, CAPEX subsidies are one-time payments, offering persistent cost benefits. However, one-off payments can pose a greater fiscal burden for the government, especially when scaling support across multiple facilities.

These findings suggest that a mix of well-targeted, transparent subsidies—particularly capital support and carbon-based incentives—can meaningfully close the cost gap between green and conventional steel, accelerating adoption while optimising public expenditure. that a mix of well-targeted, transparent subsidies—particularly capital support and carbon-based incentives—can meaningfully close the cost gap between green and conventional steel, accelerating adoption while optimising public expenditure.

Figure 8. Subsidy Amount Required per 1,000 tppa to Achieve $1 LCOS Reduction

Source: TA analysis

Source: TA analysis

Greener and Cheaper Electricity is Key

Figure 9. Provincial Green Steel Premium Relative to BF-BOF in 2030, Considering 40% Lower Grid Electricity Price and Half Emission Factor Compared to 2024

Source: TA analysis

As shown in the above analysis, reducing both the carbon intensity of grid electricity and the cost of electricity substantially lowers the LCOS of H2-DRI-EAF. With improvements in these two dimensions, considering 40% lower grid electricity price and half emission factor compared to 2024, half of the provinces analysed can achieve a green premium of less than 10%—a critical threshold for commercial viability.

China’s policy landscape is already moving in this direction. According to the notice on 2025 renewable electricity consumption targets , green power consumption quotas will be expanded beyond aluminium to include key sectors such as steel, cement, polysilicon, and data centres. Specifically, the steel industry is required to achieve a 26.2% to 70% share of renewable electricity use by 2026.

This mandatory transition toward cleaner electricity not only aligns with national climate goals but also strengthens the business case for green steel. As shown in our analysis, increased access to low-emission and competitively priced electricity would significantly benefit H2-DRI-EAF operations—enabling greater grid flexibility, reducing reliance on costly storage, and improving overall system economics.

From a policy perspective, aligning electricity decarbonisation targets with industry-specific clean energy mandates ensures that low-carbon technologies such as H2-DRI-EAF are not only technically viable but also economically competitive. By combining cleaner grids with supportive market structures (e.g., green power certificates, tiered electricity pricing), China can accelerate its transition to low-carbon steel while safeguarding energy security and industrial productivity.

Unlocking cost-competitive green steel in China through policy, innovation, and decarbonised energy systems

This analysis demonstrates that green hydrogen-based steelmaking using H2-DRI-EAF can play a critical role in China’s path to carbon neutrality. While currently more expensive than conventional steelmaking, the cost gap can be significantly reduced through a combination of technological progress, grid decarbonisation, and well-designed policy support.

Key cost drivers—including renewable energy, electrolyser systems, and storage—are expected to decline due to technological learning, especially in China where domestic manufacturing is already cost-competitive. Grid electricity’s carbon intensity and price are pivotal: provinces with cheaper and cleaner electricity can reach green premiums below 10%, making H2-DRI-EAF more commercially viable.

Government interventions will be essential to accelerate adoption. CAPEX subsidies, carbon tax credits, electricity price support, and green financing all help lower the Levelised Cost of Steel, but they differ in efficiency. Among them, capital subsidies are the most cost-effective, while interest rate reductions are the least. China’s evolving industrial policies—such as renewable energy consumption quotas and tax incentives for ultra-low-emission performance—provide a strong foundation for such support.

Ultimately, aligning energy system decarbonisation with green steel deployment, and leveraging China’s manufacturing scale and policy tools, can unlock a viable pathway toward low-carbon industrial transformation. A strategic mix of innovation, infrastructure, and incentives is key to making green steel a scalable, affordable reality in China.

Appendix

Major CAPEX components

|

Component |

Cost |

Unit |

Reference |

Supporting Documentation |

|

Wind |

576.4 |

$/kW |

CREEI |

13 |

|

Solar |

479.5 |

$/kW |

CREEI |

13 |

|

Electrolyser |

271 |

$/kW |

TA estimate |

14 15 16 |

|

H2 Storage |

962 |

$/kg |

TA estimate |

17 |

|

H2 Compressor |

206044 |

$/Unit (2000kg) |

Huaan Securities |

18 |

|

Battery |

230 |

$/kW |

TA estimate |

19 20 |

|

DR Shaft Furnace |

275 |

$/tDRI |

TA estimate |

21 22 |

|

EAF |

439 |

$/tSteel |

TA estimate |

23 24 |

Major OPEX components

|

Component |

Cost |

Unit |

|

BF grade ore (fines) |

96 |

$/t |

|

Coking coal price |

230 |

$/t |

|

DR grade ore (pellets) |

139 |

$/t |

For sensitivity analysis related to commodity prices, we welcome you to contact the authors of this report.

Endnotes

- https://globalenergymonitor.org/wp-content/uploads/2024/03/GEM-China-steel-brief-March-2024.pdf

- https://iea.blob.core.windows.net/assets/c4d96342-f626-4aea-8dac-df1d1e567135/AchievingNetZeroHeavyIndustrySectorsinG7Members.pdf

- http://www.csteelnews.com/xwzx/hydt/202407/t20240719_90410.html

- Averaged over all the provinces analysed

- Provincial grid electricity prices are not factored into this analysis

- https://link.springer.com/article/10.1007/s12140-025-09447-1?

- https://www.pv-magazine.com/2024/03/21/electrolyzer-prices-what-to-expect/

- https://www.sciencedirect.com/science/article/abs/pii/S0959652623020061

- https://transitionasia.org/storage/2025/02/Will_China_Win_the_Green_Steel_Race_241006_1.pdf

- https://www.ndrc.gov.cn/xxgk/zcfb/ghxwj/202404/t20240408_1365534.html

- https://www.gov.cn/zhengce/202406/content_6956537.htm

- https://www.gov.cn/xinwen/2021-11/08/content_5649848.htm

- http://www.creei.cn/ueditor/jsp/upload/file/20250603/1748929665756038431.pdf

- https://www.pv-magazine.com/2024/03/21/electrolyzer-prices-what-to-expect/

- https://www.metal.com/en/newscontent/103225251

- https://www.rechargenews.com/energy-transition/will-us-and-european-green-hydrogen-markets-soon-be-flooded-by-cheap-chinese-electrolysers-/2-1-1165966

- https://h2.in-en.com/html/h2-2431932.shtml

- https://pdf.dfcfw.com/pdf/H3_AP202303291584660349_1.pdf

- https://about.bnef.com/insights/clean-energy/lithium-ion-batteries-are-set-to-face-competition-from-novel-tech-for-long-duration-storage-bloombergnef-research/

- https://www.ess-news.com/2025/06/26/china-energy-engineering-launches-record-25-gwh-storage-tender-as-prices-hit-historic-low/

- https://www.sciencedirect.com/science/article/pii/S0959652618326301

- https://www.sciencedirect.com/science/article/pii/S0959652622009659

- https://www.recyclingtoday.com/news/voestalpine-austria-steel-eaf-conversion-scrap-recycling-hbi-euros/

- https://eurometal.net/salzgitter-contracts-primetals-for-eaf/

Data and Disclaimer

This analysis is for informational purposes only and does not constitute investment advice, and should not be relied upon to make any investment decision. The briefing represents the authors’ views and interpretations of publicly available information that is self-reported by the companies assessed. References are provided for company reporting but the authors did not seek to validate the public self-reported information provided by those companies. Therefore, the authors cannot guarantee the factual accuracy of all information presented in this briefing. The authors and Transition Asia expressly assume no liability for information used or published by third parties with reference to this report.

Author

Alastair Jackson

Head of Research

Lilly Qiu

Contributing Analyst and Modelling Lead