Transition Asia’s response to Nippon Steel’s proposed plans to increase share of EAF-based technology in bid to achieve net zero

May 18, 2023

Hong Kong, 18 May 2023 — Nippon Steel recently announced ahead of its 2023 annual general meeting that they would begin to study the shift from blast furnaces (BF) to electric arc furnaces (EAF). This announcement was a welcome response to investor and civil society pressure, in which Transition Asia has played a supporting role through research and engagement [1], to increase the share of EAFs in its fleet as fast as possible for 1.5°C-aligned emissions reduction efforts.

While Transition Asia commends Nippon Steel’s openness to engagement with investors and other stakeholders regarding its emissions reduction plans, we recommend that more urgent commitments be made to prevent additional carbon lock-in.

In response to the progress of the ‘Nippon Steel Carbon Neutral Vision 2050’ mentioned in the news release, we have analysed each of the three efforts outlined below and provide recommended actions for increased emissions reduction potential:

Hydrogen injection into BFs

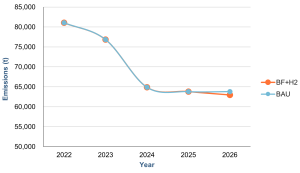

This method of emissions reduction is a derivative of the expensive and unproven COURSE50 technology. For the hydrogen injection into BFs, the East Nippon Works Kimitsu Area BF was relined in 2012, and there is no mention of carbon capture storage (CCS) technology. This effort has a maximum 10% reduction via hydrogen compared to BF operation as usual if CCS is not included. It is a likely scenario that CCS is proving to be too technologically and economically challenging due to low BF CO2 concentrations, amine volatility, and the additional energy requirements for the equipment.

This method of emissions reduction is a derivative of the expensive and unproven COURSE50 technology. For the hydrogen injection into BFs, the East Nippon Works Kimitsu Area BF was relined in 2012, and there is no mention of carbon capture storage (CCS) technology. This effort has a maximum 10% reduction via hydrogen compared to BF operation as usual if CCS is not included. It is a likely scenario that CCS is proving to be too technologically and economically challenging due to low BF CO2 concentrations, amine volatility, and the additional energy requirements for the equipment.

Integration of this new technology into the Kimitsu Area BF—which makes up around 10% of total production—would only result in a group annual emission reduction of 1-2% in 2026 compared to our business-as-usual (BAU) scenario (see figure). Note that this reduction is the maximum fixed amount; Nippon Steel can only reduce its emissions further in the long term by shifting its BFs to EAFs, integrating the use of DRI and scrap, and increasing the use of RE.

Recommendation:

-

-

- As CAPEX requirements for COURSE50 are still unknown, despite the project starting in 2008, and the limited decoupling ability of adding expensive technology to BFs, we recommend that investors seek more clarity on CAPEX requirements to assess whether this effort represents long-term value where low-carbon steel products and financed emissions are increasingly coming under scrutiny.

-

Hydrogen direct reduction of iron (H2-DRI)

Nippon Steel’s H2-DRI development remains a small-scale R&D concept at the Hasaki R&D Center as of now. On the contrary, its international peers Thyssenkrupp and SSAB are planning to commercially produce millions of tons of H2-DRI by 2026 with Japanese-owned equipment and 100% green hydrogen, respectively.

Recommendation:

-

-

- Nippon Steel should explore collaboration opportunities with established plant providers such as Tenova and Midrex to deliver at-scale H2-DRI solutions.

-

High-grade steel production in large-sized EAFs

The commercial operation of Setouchi Works Hirohata Area is a positive step forward, but is a delayed step for such a large company. Technological advances have ensured that the differences in steel produced from either a BF or EAF are almost imperceptible. Nippon Steel’s feedstock for the Hirohata continues to be high-grade home scrap (unused steel from steel processing) that has never left the plant and pig iron from BFs. Unless replaced with low-emission iron or steel, these high-emission feedstocks will hinder any major efforts to reduce emissions.

Additionally, the company highlights that it is the first to enable an integrated EAF to produce high-grade electrical steel sheets, but doing this is quite novel. Electrical steel is a relatively niche type of steel that is particularly suited to specific parts (motor, generator, etc.) of electric vehicles (EV), and its soft magnetic properties and high investment barrier make it unsuitable for most uses of steel. This type of steel makes up only a small portion of Nippon Steel’s current production and sales, and does not have a high decarbonisation effect.

Nippon Steel has the opportunity to power its large-scale EAFs through power purchase agreements (PPAs). Solar PV’s levelised cost of energy (LCOE) is expected to stay lower than the price of fossil fuels going forward and get even cheaper over time. The price of power from large-scale solar is estimated to be around JPY 8.5/kWh in 2050 while the cost of power from coal is to remain around JPY 12-13/kWh from 2030-2050.

Recommendations:

-

-

- Establish a credible plan to incorporate other feedstocks in the forms of other grades of scrap, DRI or hot briquetted iron (HBI). Additional improvements should also focus on obsolete scrap processing technologies.

- Seek to produce significant proportions of their current products via EAFs, utilising subsequent steel production facilities to enable efficient plant transformation.

- Utilise a solar PV LCOE lower than the average national grid tariff to source emission-free electricity to power EAFs via PPAs. Although the use of virtual PPAs carries balance sheet implications for the company, we believe this can be easily overlooked by investors.

-

“Nippon Steel has not yet released updated emissions reduction data and, as it stands, the company remains far off a 1.5°C trajectory if it is only implementing these incremental improvements,” comments Lauren Huleatt, Transition Asia’s Program Manager. “While we welcome the steps in the right direction that are being taken, the company needs to commit to rapid and ambitious climate action within this decade by looking into several available and proven green solutions.”

-Ends-

[1] Transition Asia has previously published analyses of Nippon Steel’s emissions pathways, peer comparison of Nippon Steel and JFE Holdings, and the Japanese steel industry’s decarbonisation solutions. Most recently, we have modelled Nippon Steel’s options for H2-DRI-EAF and H2-DRI-HBI-EAF (also available in Japanese) to support our continued engagement with Nippon Steel and its investors.

Notes to editor

- Transition Asia’s detailed recommendations for Nippon Steel and its stakeholders ahead of its 2023 AGM are available here.

- Transition Asia’s Steel Explainer is available in English, Japanese and Simplified Chinese.

For more information, or exclusive interviews, please contact:

Crystal Chow, Communications Specialist

+852-93015004

About Transition Asia

Founded in 2021, Transition Asia is a Hong Kong-based non-profit think tank that focuses on driving 1.5°C-aligned corporate climate action in East Asia through in-depth sectoral and policy analysis, investor insights, and strategic engagement. Transition Asia works with corporate, finance, and policy stakeholders across the globe to achieve transformative change for a net-zero, resilient future. Visit transitionasia.org or follow us @transitionasia to learn more.