Japan’s Green Steel Transition: Green Iron EAFs, Carbon Pricing & Renewable Electricity

Key Takeaways

- The implementation of Japan’s GX-ETS in FY2026 will fundamentally shift the cost dynamics of the green H2-Iron–EAF route as the costs of carbon-intensive BF–BOF steel are inflated. To drive cost competitiveness, domestic benchmarks must evolve toward international standards to ensure that green H2-Iron–EAF steel abatement costs are reduced.

- Renewable electricity remains largely cost-prohibitive for EAF operations due to a structural disconnect: the intermittent, solar-heavy PPA market is ill-suited for steel mills’ continuous load requirements. High PPA costs and steelmakers’ reluctance to commit to ill-matched, long-term contracts underscore the need for sustained grid decarbonisation as a strategic prerequisite for the EAF pathway to remain an economically robust and green solution.

- Utilising fossil-based captive power such as LNG to bypass current grid-based emissions creates long-term carbon liabilities for companies and government. Grid reliance remains the superior decarbonisation path, as declining grid emission factors will eventually outperform static fossil-based solutions.

- Regional green iron sourcing is a critical cost lever. HBI produced in the Middle East, leveraging superior renewable resources and cheap plant fabrication, is currently USD 258 per tonne cheaper than imports of green iron from Australia.

- The Japanese steel transition requires an integrated framework that simultaneously addresses carbon pricing, renewable energy, and market-side demand. Isolated interventions are insufficient to trigger the system-level shift required for steel sector electrification.

Introduction

The Japanese steel industry is responsible for around 15% of the country’s total CO2 emissions, making it one of the most carbon-intensive sectors and highlighting the urgent need for rapid and effective decarbonisation measures. To accomplish this, electric arc furnaces (EAF) are widely seen as the most viable short-term solution, and major blast furnace (BF) steelmakers such as Nippon Steel and JFE have begun to announce plans to convert some of their BFs into EAFs.

From FY2026, Japan will implement the second phase of its emissions trading scheme (GX-ETS), requiring participation from companies emitting more than 100,000 tCO2 annually, including BF and EAF steelmakers. While the specifics of this scheme are still being discussed by government councils, depending on the carbon price, EAF steel could potentially become sufficiently competitive against BF steel to warrant an expedited market transition.

This paper compares two primary steel production routes: the conventional brownfield BF–BOF process and the use of green H2-Iron in greenfield EAFs, to assess the level of carbon pricing or benchmark setting that may be required under the second phase of the GX-ETS to incentivise the deployment of greenfield EAFs using green H2-Iron.1

Carbon pricing trends and Japan's carbon policies

The expanding global reach of carbon pricing

Globally, around 80 carbon pricing mechanisms have already been introduced, covering around 28% of total greenhouse gas (GHG) emissions.2 While uptake was initially concentrated in advanced economies such as the EU, the number of schemes in emerging economies has grown in recent years, with further expansion anticipated. Current carbon prices differ widely between countries, ranging from USD 0.1 to 159/tCO2, with generally higher prices observed in developed economies.2 Across jurisdictions that have implemented carbon pricing, the global average now stands at around USD 19/tCO2, roughly double the level of ten years ago, and is expected to rise further.3 In industry, including steelmaking, carbon pricing already applies to 43% of global emissions, second only to the power sector, illustrating the extensive implementation of such schemes in industrial sectors.2

Under the EU ETS, steel producers within the EU have historically received free allocation of emission allowances to maintain their competitiveness against producers in regions without carbon pricing.4 This has prevented domestically produced steel from becoming disproportionately expensive relative to imports. However, from 2026, the introduction of the Carbon Border Adjustment Mechanism (CBAM), which imposes a carbon price on imported products equivalent to that faced by EU producers, will see these free allocations gradually phased out. As a result, non-EU steelmakers exporting to the EU will also be subject to EU carbon prices.

Furthermore, the European Steel and Metals Action Plan, released in March 2025, proposes extending CBAM coverage for steel to downstream products.5 If implemented, this could affect automobiles, home appliances, and other goods imported into the EU that contain steel produced outside the bloc. In 2024, Japan exported around 1.36 Mt of steel to the EU.6 In addition, around 420,000 vehicles were exported that year. According to the Japan Automobile Manufacturers Association each vehicle contains an average of 1.5 tonnes of steel.5 7 On this basis, the total volume of steel exported to the EU, either as raw material or embedded in vehicles, is estimated near 2 Mt. Including ETS coverage to the steel embedded in other downstream products, such as electrical appliances and machinery, would raise the total further. Accordingly, extending CBAM to downstream products could increase the amount of Japanese steel subject to the mechanism by around 46%, creating a potentially significant additional impact for Japan.

Carbon pricing does not only exert a direct impact in proportion to a company’s emissions; it can also bring about indirect effects through rising electricity prices. In South Korea’s K-ETS, for instance, the share of paid auctioning in the power sector is increasing, which is expected to raise electricity prices by KRW 9.8/kWh (USD 0.007/kWh), illustrating how carbon pricing can impose additional cost burdens on the steel mills reliant on grid electricity.8

Carbon pricing has both direct and indirect implications for the steel industry, and these effects can extend across borders. To maintain and enhance the industry’s international competitiveness, it is essential that Japan’s domestic carbon pricing systems are designed with close attention to developments in other countries and regions.

Across jurisdiction that have implemented carbon pricing, the global average now stands at around USD 19/tCO2, roughly double the level of ten years ago

Extending CBAM to downstream products could increase the amount of Japanese steel subject to the mechanism by around 46%

Japan’s “Pro-Growth” Carbon Pricing Approach

As part of Japan’s effort to achieve carbon neutrality by 2050, the government has adopted the Basic Policy for the Realisation of GX in February 2023. This sets out a “Green Transformation” (GX) strategy aimed at shifting the country’s industrial and social structures away from heavy dependence on fossil fuels and toward an economy centred on clean energy. As a core element of this strategy, “pro-growth carbon pricing” model has been introduced.9 10 Under this framework, the government will provide around JPY 20 trillion (USD 13 billion) in upfront support over the first ten years through the issuance of GX Economy Transition Bonds. These funds will be channelled into investments that contribute both to decarbonisation and to economic growth, with revenue from carbon pricing intended to serve as the source of repayment. Cumulative government revenue from carbon pricing is therefore expected to exceed JPY 20 trillion. In this respect, Japan’s carbon pricing system places strong emphasis on linking decarbonisation with economic growth, giving it distinct character compared with schemes such as the EU ETS, which place primary emphasis on emissions reductions.

Within this system, from FY2026, companies with direct emissions exceeding 100,000 tonnes of CO2 per year will be required to participate in the GX-ETS, which is expected to cover roughly 60% of Japan’s total emissions. In addition, partial paid auctioning of allowances is scheduled to begin in FY2033, starting with the power sector. The steel industry, particularly BF steelmakers, will fall within the scope of the GX-ETS, meaning they will face not only direct compliance costs but also indirect cost increases through higher electricity prices, especially once paid auctioning begins in the power sector. No details have yet been released on whether paid auctioning will later be extended to other sectors, including steel, or when such a change might occur.

In addition to the GX-ETS, from FY2028, a fossil fuel levy will also be introduced. This will apply to importers of fossil fuels, who will be charged according to the volume of CO2 emissions associated with the fuels they bring into Japan. Unlike the GX-ETS, which targets large domestic emitters, the levy is designed to place a price on the carbon content of imported fuels at the point of entry.

Under the ETS, energy-intensive sectors such as the steel industry are expected to adopt a benchmarking approach on a company basis. Based on published discussions to date, the government intends to prioritise a smooth and orderly launch of the scheme. Accordingly, benchmarks are expected to be set at the emissions intensity level of the top 50% of performers within each industry at the outset, tightening to the top 32.5% by FY2030.11 In practice, this would reduce the upstream emissions of BF–BOF from 2.11 tCO2/t to 2.09 tCO2/t (around 1%) and of EAF from 0.073 tCO2/t to 0.064 tCO2/t (around 4.5%) over five years.12 These figures are derived not from Japan’s NDC but from empirical evidence suggesting that Japanese companies have historically taken around a decade to improve their emissions intensity to the top 15% within their industry.

By comparison, the EU ETS uses a benchmark based on the top 10% of installations, while Korea’s K-ETS uses the top 20%. Given that Japan’s benchmark is comparatively less stringent, Japanese steel products may still incur partial carbon costs under foreign schemes, including CBAM, even after the introduction of domestic carbon pricing.13 Under EU-CBAM’s crediting mechanism, any carbon costs paid under Japan’s GX-ETS would be deducted from the CBAM liability; however, any remaining gap between the GX-ETS benchmark and the (currently) more stringent EU benchmark would still need to be settled.

Moreover, unlike the EU-ETS and K-ETS, no aggregate emissions cap has yet been set for participating companies, raising concerns that the scheme’s overall mitigation impact may be limited.14 Reflecting the scheme’s emphasis on economic growth alongside emissions reduction, questions remain as to whether the current design will be sufficient to ensure alignment with Japan’s NDC targets.15

The steel industry will fall under the GX-ETS, facing both direct compliance costs and indirect cost pressures from higher electricity prices

Japanese steel products may still incur partialcarbon costs under foreignschemes, including CBAM, even after the introduction of domestic carbon pricing

Carbon pricing implications for Japanese steel mills

Carbon prices do not affect steel producers uniformly; the impact depends on factors such as process emissions intensity, exposure to electricity costs, and the availability of lower-carbon options like green H2-Iron. The following analysis compares the production costs of the BF–BOF process with those of a green H2-Iron–EAF system, specifically focusing on hot briquetted iron (HBI) or pig iron produced using green hydrogen. This includes an estimation of import costs for green iron sourced from three potential nations: Australia, Saudi Arabia, and the United Arab Emirates (UAE).

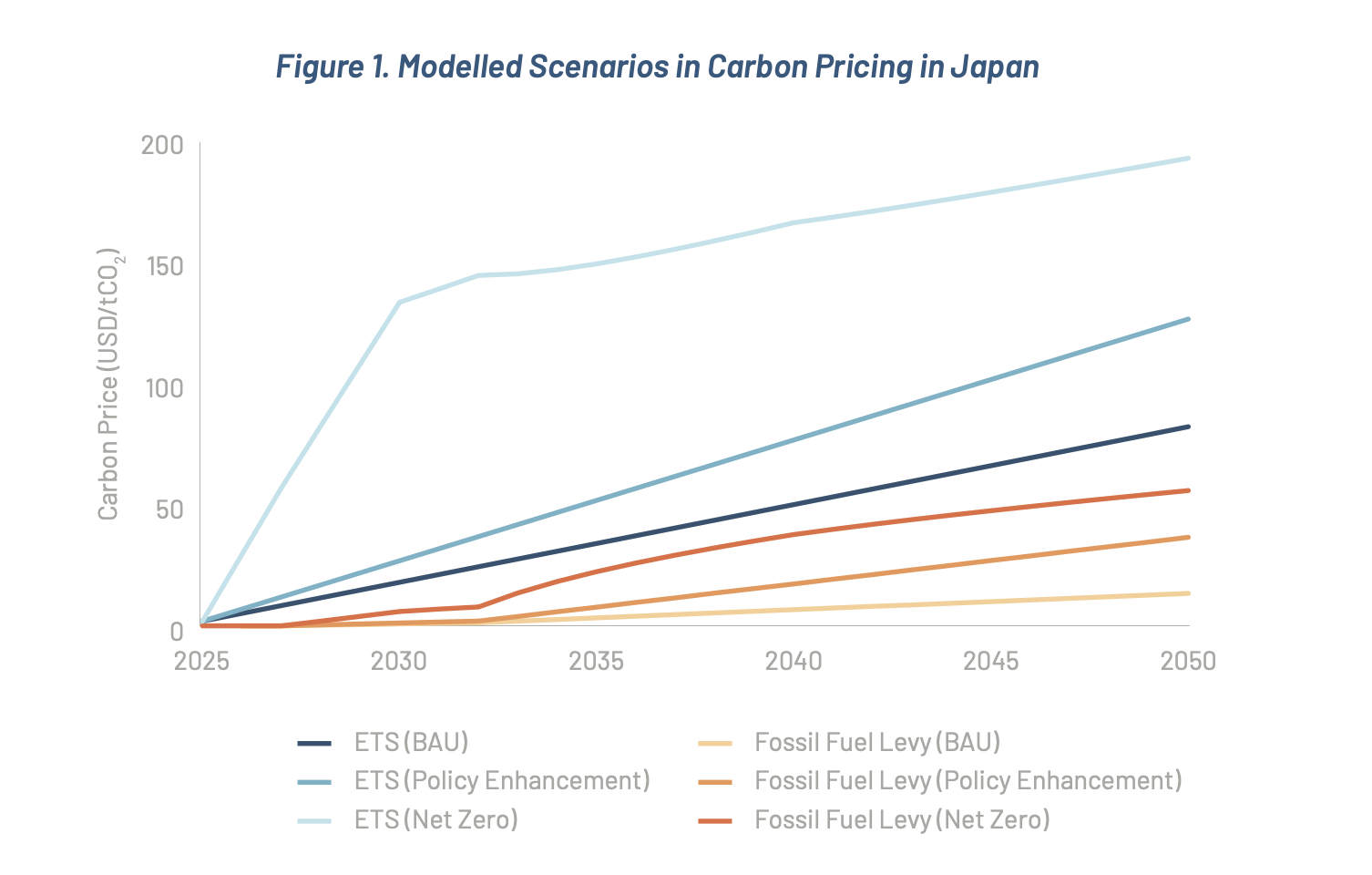

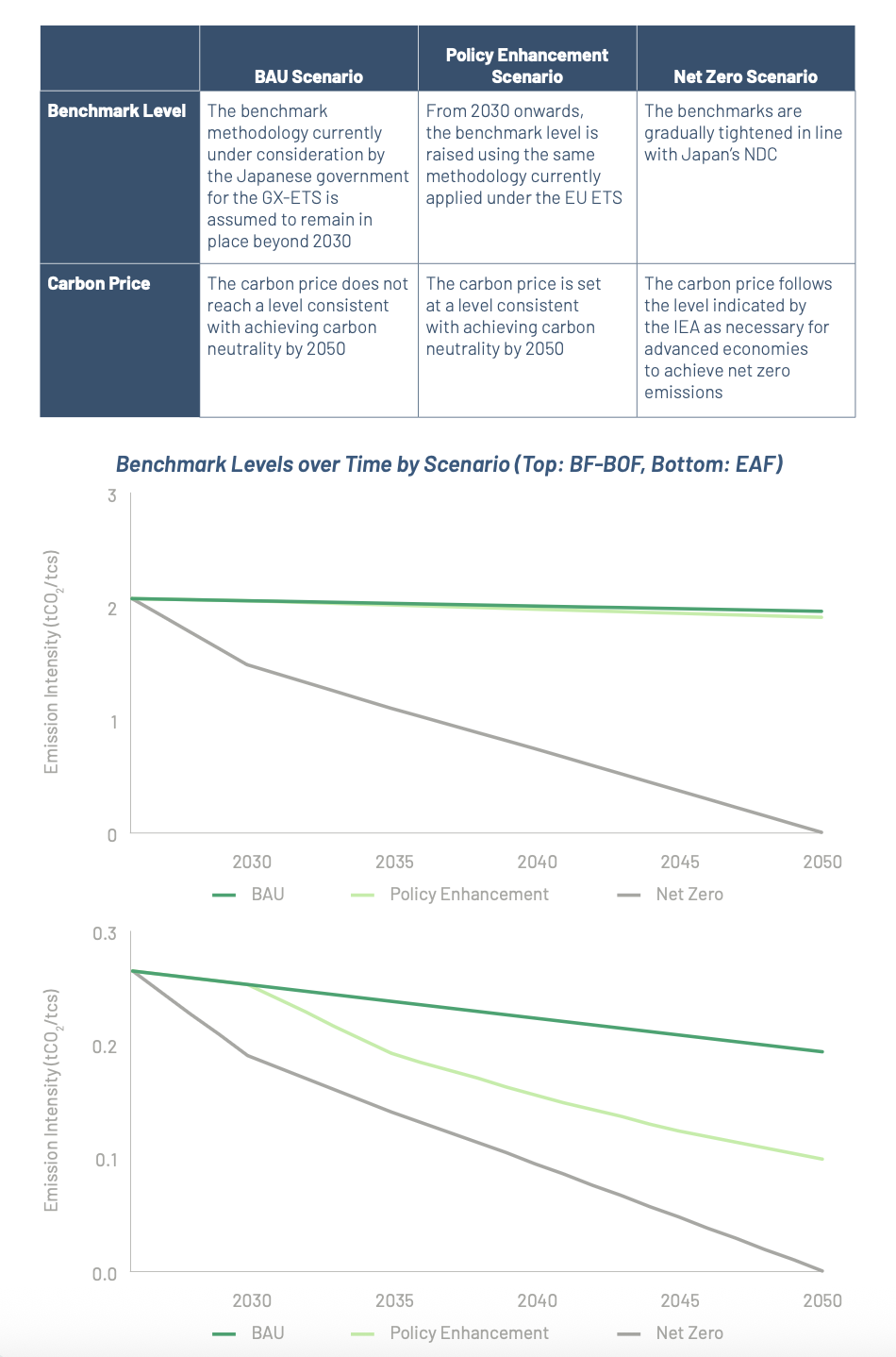

Three ETS and fossil fuel levy scenarios are modelled: the Business-as-Usual (BAU) scenario, the Policy Enhancement scenario, and the Net Zero scenario.16 17 Under the BAU Scenario, benchmarks remain largely unchanged, and carbon prices stay below those consistent with achieving net zero, reaching only a 70% reduction in emissions from FY2030 by 2050, resulting in limited pressure to decarbonise. The Policy Enhancement Scenario introduces tighter benchmarks and a carbon price aligned with Japan’s 2050 neutrality target, signalling stronger regulatory ambition. The Net Zero Scenario applies progressively stricter benchmarks in line with Japan’s NDC and carbon prices at levels indicated by the IEA for advanced economies.

Source: TA analysis

Electricity and the impact of carbon prices

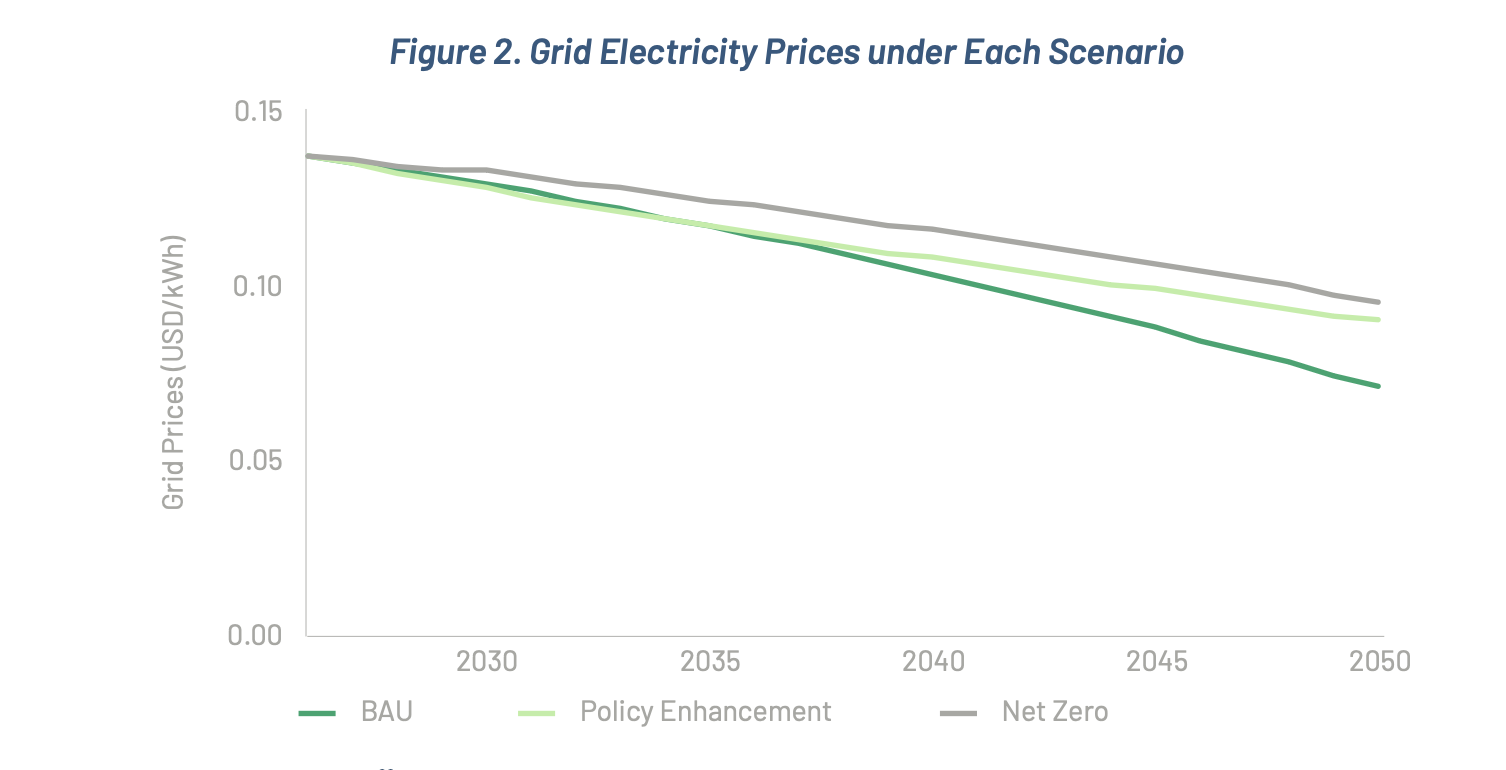

Figure 2 shows the projected prices of grid electricity under each scenario. These projections draw on current grid prices; the Ministry of Economy, Trade and Industry’s (METI) published generation costs and power mix for the present and 2040; and scenario-specific carbon prices. 18 19 20 21 As the share of RE increases and costs continue to decline, grid electricity prices are expected to fall to some extent. However, the continued use of fossil fuels means that grid electricity will remain subject to carbon pricing, so the more ambitious the carbon pricing scheme, the smaller the degree of price reduction.

Source: TA analysis22

Continued use of fossil fuels means that grid electricity will remain subject to carbon pricing,so the more ambitious the carbon pricing scheme, the smaller the degree of price reduction

Renewable electricity procurement constraints in Japan’s steel industry

Domestic BF steelmakers acknowledge that decarbonising electricity is essential to achieving carbon neutrality. They also recognise that switching to EAFs will substantially increase power demand, necessitating both an expansion of grid capacity and a reliable supply. Nevertheless, in practice, nuclear power and alternative fuels such as hydrogen and ammonia appear to be prioritised over RE by BF steelmakers.22 23 This reflects persistent concerns about supply stability, as well as the high cost of RE procurement in Japan.

Japan’s RE costs remain among the highest in the world, with METI estimating 2023 levelised costs at USD 0.07/kWh for solar PV and USD 0.12/kWh for onshore wind.24 High land costs, administrative burdens, and grid connection constraints are major contributors. These structural factors also shape the PPA market: On-site PPAs: ~USD 0.089/kWh, Physical PPAs: ~USD 0.142/kWh, Virtual PPAs: ~USD 0.159/kWh.25

Japan offers multiple RE procurement mechanisms consistent with established GHG accounting standards, including Energy Attribute Certificates (EACs), physical and virtual PPAs, and on-site renewable installations. These options differ primarily in terms of additionality, or the extent to which procurement leads to new RE capacity. Unbundled certificates are generally associated with low additionality, while on-site RE and PPAs tied to pre-final investment decision (FID) projects offer much clearer evidence of driving new RE buildout. Non-Fossil FIT Certificates remain at similar levels to European Guarantee of Origin prices, at around USD 3/MWh, but analysts caution that demand is likely to increase as the GX-ETS starts, potentially leading to a much tighter supply–demand balance and materially higher certificate prices over time.26 27

Over time there has been increasing scrutiny of EACs, including of Japan’s non-fossil certificates; many stakeholders now see renewable energy PPAs as a more reliable, robust and transparent decarbonisation option. However, interviews conducted by Transition Asia indicate that Japanese EAF steelmakers have so far been reluctant to commit to PPAs at scale.28 This hesitation reflects not a lack of awareness of their environmental value, but rather practical constraints related to cost, structure, and operational suitability.

A key challenge is that Japan’s PPA market is dominated by small-scale, solar PV–based projects, typically structured as pay-as-produced contracts. Electricity is therefore supplied only when the asset generates electricity, regardless of whether this aligns with the buyer’s demand profile. Solar generation in Japan is concentrated within approximately 10–11 daylight hours, creating a significant mismatch for energy-intensive industries with stable or near-continuous loads.

For EAF steelmakers, this mismatch is especially problematic. EAF electricity use is relatively stable and concentrated around consecutive melts, carried out to maximise operational efficiency. Because solar-only PPAs deliver power unevenly, they offer limited ability to match the consistent load profile of an EAF, making it difficult for steelmakers to use PPAs to materially reduce emissions or meaningfully hedge electricity prices.

Cost and risk considerations further discourage early PPA adoption. Steelmakers are wary of locking in relatively high PPA prices for 10 years or more, particularly in a market where electricity prices are widely expected to decline over time. This uncertainty is compounded by the lack of clarity around Japan’s future carbon pricing trajectory. Without credible long-term signals on carbon costs, producers remain unsure whether committing to PPAs now, or delaying procurement, will ultimately prove more economically rational.

Demand-side factors also play a role. Even where steelmakers apply a price premium to RE-based steel products, this added value is not yet widely recognised by downstream sectors such as construction and automotive manufacturing. Beyond voluntary Scope 3 reduction efforts, buyers currently have limited incentives to pay for greener steel. This weak demand signal reduces the commercial case for steelmakers to absorb higher electricity costs through long-term RE procurement.

Scalability, by contrast, presents an even greater obstacle. This is because EAFs are extremely power-intensive, requiring around 650 kWh of electricity to process HBI, thereby making the scale of RE procurement a far more pressing challenge. Expanding RE generation capacity is therefore a critical prerequisite. With that being said, Japan already has examples of virtual PPAs aggregating output from multiple solar PV sites to supply data centres, demonstrating that large consumers can, in principle, mobilise sufficient renewable capacity when clear demand signals exist.29

To accelerate RE uptake in the steel sector, government policy will play a critical role. Support for cost reductions, particularly in offshore wind, which offers more stable and scalable generation profiles than solar PV, will be essential. Equally important is enabling industrial consumers to procure large-scale RE more easily, whether through aggregation mechanisms or improved grid access. Historically, RE deployment in Japan has responded to clear demand from consumers; strengthening these signals within the steel sector could therefore catalyse further investment.

Given these constraints, PPAs in their current form offer limited value for steelmakers seeking large, reliable volumes of RE. As a result, grid decarbonisation becomes even more critical. A lower-carbon grid would directly reduce the emissions intensity of green H₂-Iron–EAF steelmaking and increase the likelihood that Japanese steel will be recognised as genuinely “green.”

Japan’s RE costs remain among the highest in the world,…high land costs, administrative burdens, and grid connection constraints are major contributors

Japan already uses aggregated virtual PPAs from multiple solar PV sites to supply data centres, showing that large consumers can mobilise sufficient renewable capacity when demand signals are clear

RE-PPA prices compared to future grid developments

With the prices of virtual PPAs (USD 0.159/kWh) typically remaining constant over the course of a PPA contract, electricity supplied under a 100% RE PPA would remain more expensive than grid electricity.30 As a result, in 2032 the cost would be higher than that of grid-based electricity by USD 21/tcs under the BAU scenario, and by USD 20/tcs and USD 18/tcs under the Policy Enhancement scenario. As carbon pricing becomes more stringent, additional costs are increasingly passed through to grid electricity prices. Over time, however, the decarbonisation of the power grid reduces the emissions intensity of electricity, partially offsetting these price increases. At the same time, falling generation costs from new low-cost RE projects and the restart of existing nuclear reactors are expected to reduce average grid electricity prices. This dynamic widens the price differential between grid electricity and higher-cost RE procurement options, such as PPAs.

Source: TA analysis31

Moreover, companies are likely to enter into PPAs only where they deliver tangible benefits, either through materially lower electricity costs or higher achievable product prices. The current scenario in which PPA electricity continues to be more expensive, or is not competitive enough against grid electricity, is a clear barrier for PPA uptake across industrial players.

Falling generation costs from new low-cost RE projects and the restart of existing nuclear reactors are expected to reduce average electricity price

Fossil-based electricity for new EAF projects

Not all steelmakers in Japan are seeking grid or RE solutions. Some are pursuing EAF deployment through fossil-based electricity solutions, highlighting the potential risks of lock-in and misalignment with longer-term grid decarbonisation trends. Nippon Steel has announced that when converting the Yawata BF into an EAF (scheduled to begin operations in the second half of FY2029), it will construct four new LNG-fired power plants (total capacity 2,000 MW) to supply the EAF.32 The LNG plants are expected to become operational around 2031. The company claims this will halve the emissions factor of its electricity from the current 0.73 kgCO2/kWh and eventually aims to co-fire with hydrogen and ammonia, ultimately switching to 100% hydrogen or ammonia to achieve zero emissions.33 However, while the LNG-fired plant would reduce emissions compared with the company’s existing facilities, Japan’s grid emission factor had already fallen to 0.421 kgCO2/kWh in FY2023 and is expected to decline further as more RE comes online.34 Consequently, the relative emissions advantage of relying on LNG rather than grid electricity is unlikely to remain significant over the longer term. Moreover, the company itself projects that hydrogen and ammonia co-firing and full fuel switching will not begin until after 2040, meaning there will be little change in the emissions factor in the intervening period. In other words, for at least the next decade, Nippon Steel’s new EAFs may be unable to realise their full decarbonisation potential and will remain exposed to the impact of carbon pricing under the ETS, in addition to locking in unnecessary carbon emissions.

For at least the next decade, Nippon Steel’s new EAFs may be unable to realise their full decarbonisation potential and will remain exposed to the impact of carbon pricing under the ETS

Evaluating Production Sensitivity to Regulatory Carbon Costs

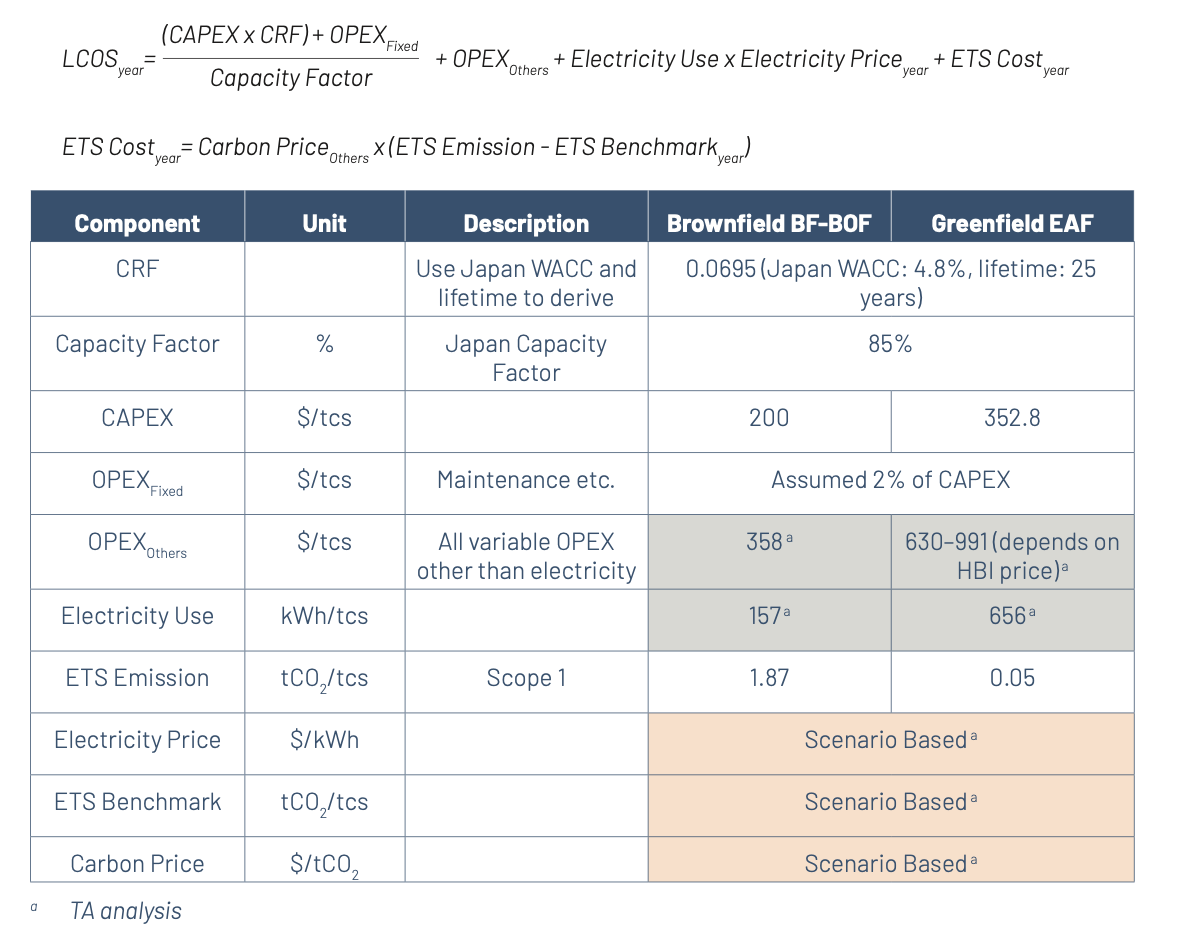

This section presents the levelised cost of steel (LCOS) in FY2032, corresponding to the end of Phase 2 of the GX-ETS, when the full free allocation of allowances to the power sector is scheduled to cease.

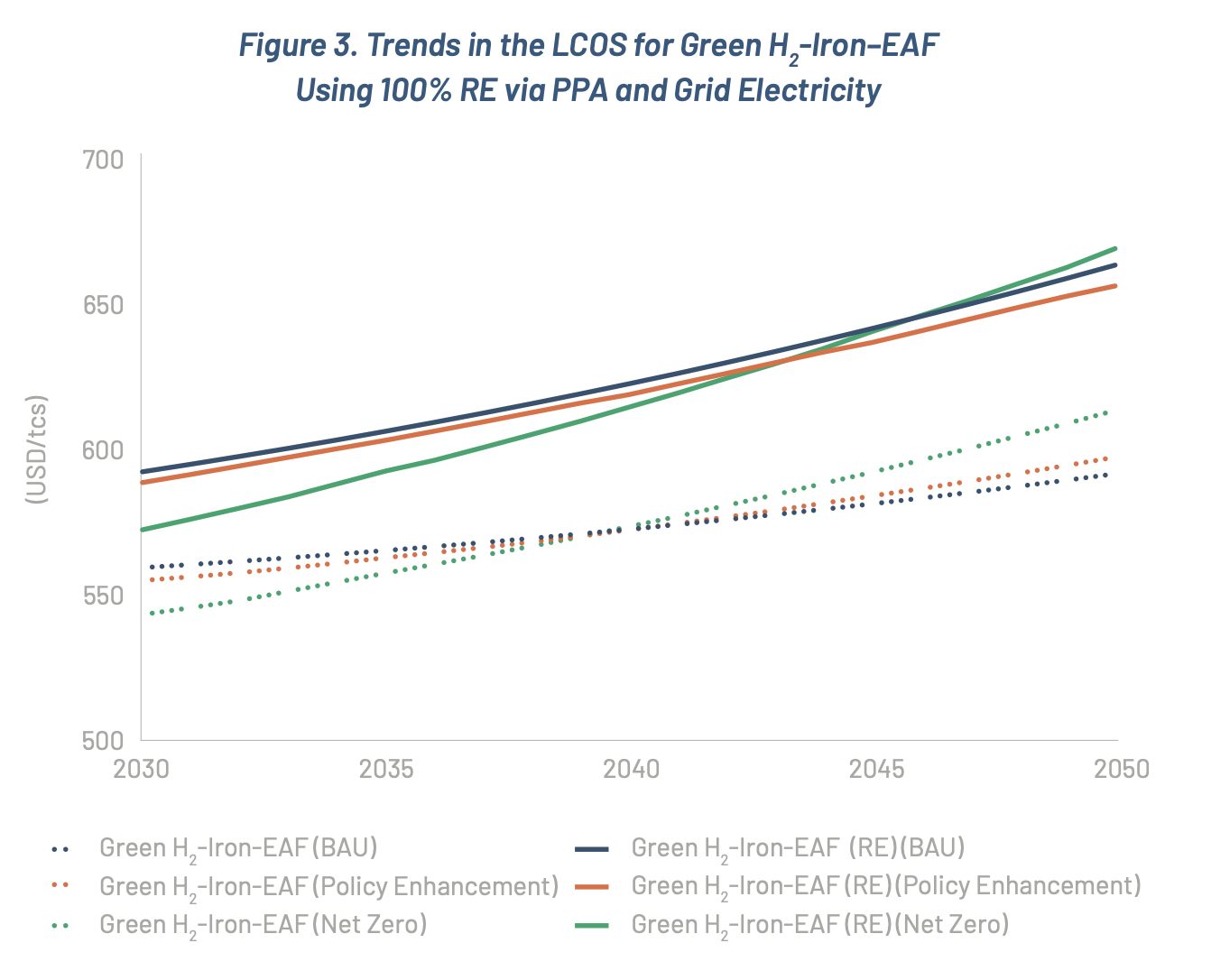

In 2032, green H2-Iron–EAF benefits from having emissions below the benchmark and from higher carbon prices under more ambitious carbon pricing frameworks. As a result, when grid electricity is used, the LCOS of green H2-Iron–EAF decreases by around USD 4/tcs under the Policy Enhancement scenario and by approximately USD 13/tcs under the Net Zero scenario relative to BAU. When LNG-fired electricity is used, the LCOS also declines by around USD 3/tcs under the Policy Enhancement scenario and by approximately USD 6/tcs under the Net Zero scenario. These results indicate that green H2-Iron–EAF relying on grid electricity is less exposed to carbon pricing impacts than when LNG-fired power is used.

For BF-BOF based steel, the LCOS remains largely unchanged under the Policy Enhancement scenario and by roughly USD 82/tcs under the Net Zero scenario. The more ambitious the carbon-pricing framework, the greater the impact on BF–BOF relative to green H2-Iron–EAF. The reason is that around 77% of green H2-Iron–EAF emissions are Scope 2, whereas BF–BOF emissions are predominantly Scope 1 and therefore directly covered by the ETS. With carbon prices expected to rise year on year, the persistently high and relatively constant emissions intensity of BF–BOF makes further cost escalation unavoidable.

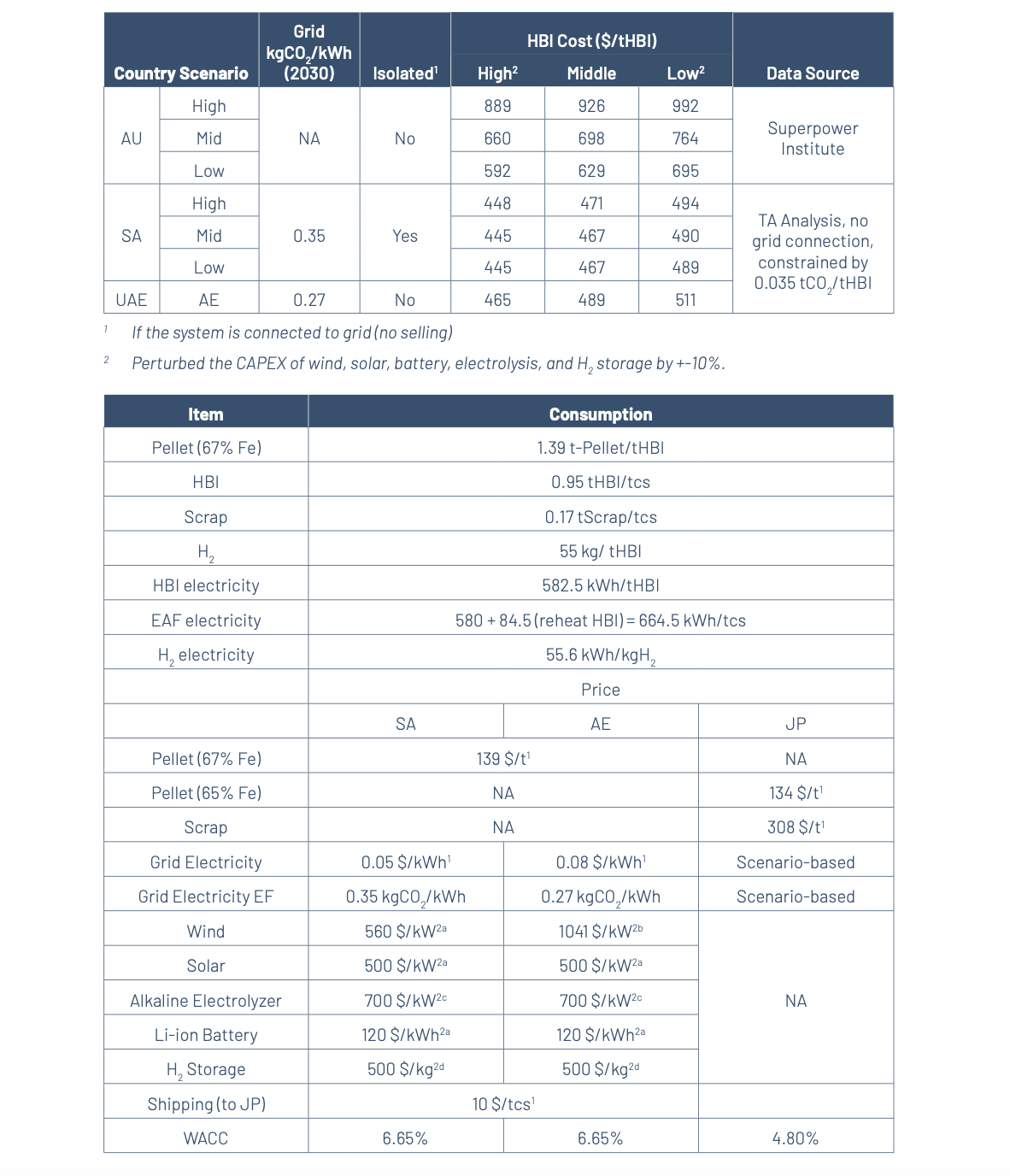

The cost of green H2-Iron–EAF varies by scenario and by region, ranging from USD 570–1,095/tcs. LNG-based green H2-Iron–EAF is more expensive than grid-based green H2-Iron–EAF by at least USD 8/tcs. Among the three supplier countries, imports from Saudi Arabia are the least expensive on average, around USD 258/tcs cheaper than those from Australia, the highest-cost supplier. Costs in Australia, however, show considerable variation, meaning that under certain conditions some regions could be competitive with other supplier countries.

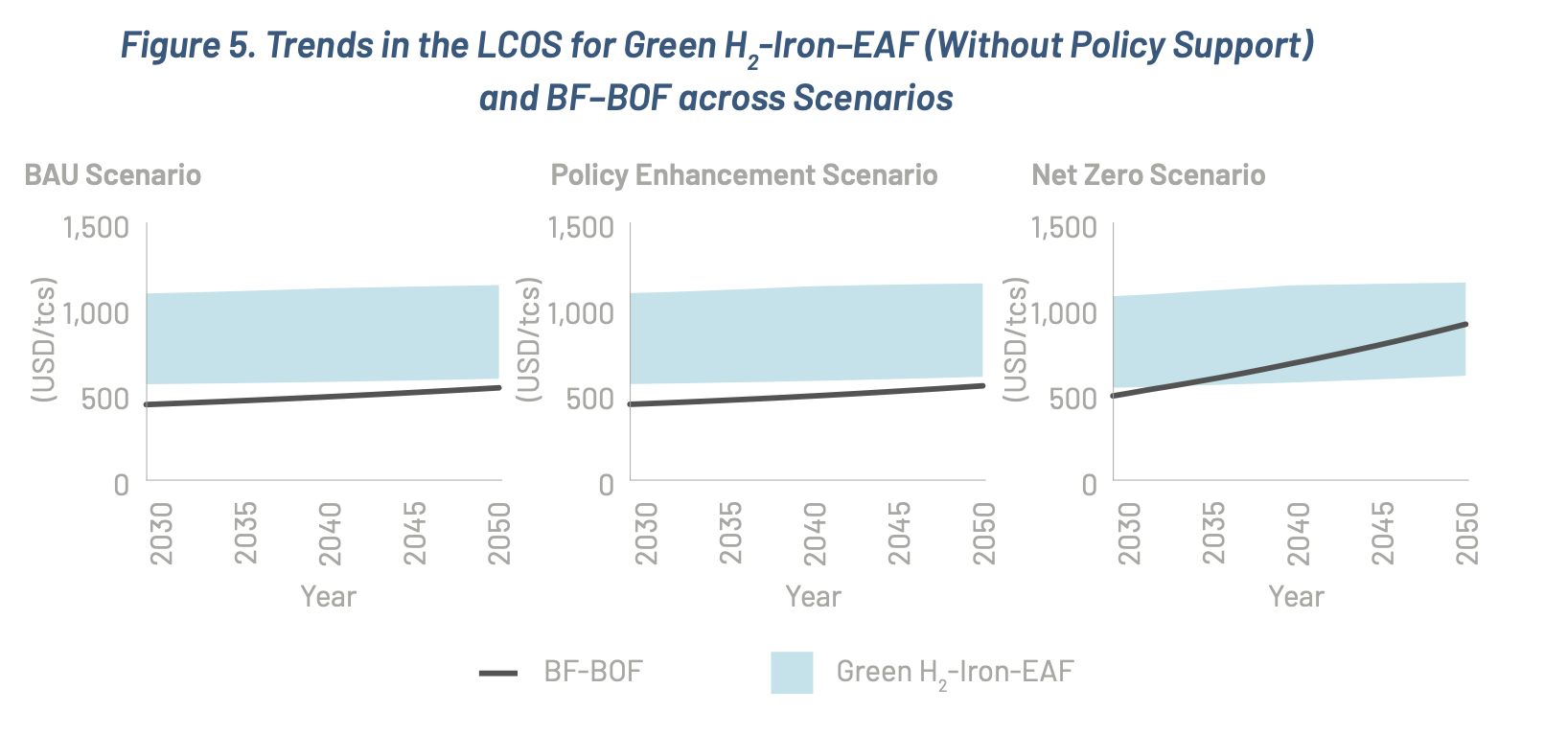

Without policy incentives, green H2-Iron–EAF remains more expensive than BF–BOF across all scenarios and import regions. Under the BAU and Policy Enhancement scenarios, the cost premium relative to BF–BOF is at least 30–93% (approximately USD 135–412/tcs). Under the Net Zero scenario, however, the premium is reduced to around USD 39–317/tcs, equivalent to roughly 7–60%. This range is comparable to, or lower than, the price premiums currently charged for low-carbon steel produced by BF steelmakers using mass-balance-based approaches. Given that mass-balance-based steel is not recognised as “green” under the current EU CBAM framework, steel produced via green H2-HBI–EAF is likely to be viewed as attractive by buyers.37

Policy support, in addition to carbon pricing, significantly helps to reduce the cost difference. Japan, for instance, offers substantial incentives for low-carbon steel production. These include the Strategic Field Domestic Production Promotion Tax System, which grants a tax credit of JPY 5,000–20,000 (roughly USD 33–130) per tonne of steel for a decade when transitioning from BF–BOF to EAF technology. Furthermore, the Energy and Manufacturing Process Transformation Support Business (Business I (Steel)) subsidises up to one-third of capital expenditure. 38 39

Under this latter programme, major companies have received significant funding:

- JFE Steel has been approved to receive up to JPY 104.5 billion (around USD 0.7 billion) for converting to an EAF with an approximate annual capacity of 2 Mt.40

- Nippon Steel has been approved to receive up to JPY 251.4 billion (around USD 1.7 billion) for EAF investments totaling about 2.9 Mt per year.41

Our analysis indicates that these policy incentives could improve the cost competitiveness of green H2-Iron–EAF steel by up to approximately USD 80 per tonne of crude steel (tcs).

Source: TA analysis35 , Superpower Institute36

Despite this policy support, the average cost of green H2-HBI–EAF remains higher than BF–BOF under the BAU and Policy Enhancement scenarios, by around 12–75% (approximately USD 53–332/tcs). Under the Net Zero scenario, however, outcomes diverge by region: in Australia, costs remain around 45% (USD 237/tcs) higher than BF–BOF, whereas in Saudi Arabia and the UAE, green H2-HBI–EAF becomes around 4–8% (USD 21–41/tcs) cheaper than BF–BOF. This implies that, with strong policy support and under a highly ambitious carbon pricing framework, green H2-HBI–EAF could achieve cost parity with, or even outperform, BF–BOF steel, falling below the typical premiums associated with mass-balance-based low-carbon steel and thereby gaining more favourable market acceptance.

Although its “green” credentials are globally acknowledged, the green H2-HBI–EAF steel production pathway is forecast to retain a cost disadvantage compared to the conventional BF–BOF methodology across all import territories until at least 2032. This situation highlights the need for substantial cost reduction, particularly within HBI production. Nevertheless, this cost disparity could be considerably mitigated, or even eliminated under a net zero scenario, contingent upon the implementation of suitable policy incentives and more stringent carbon pricing mechanisms. Such a cost reversal would be instrumental in increasing the acceptance of green H2-HBI–EAF steel among institutional purchasers.

With strong policy support and under a highly ambitious carbon pricing framework, green H2-HBI-EAF could achieve cost parity with, or even outperform, BF-BOF steel

Source: TA analysis

The cost of green H2-Iron–EAF steel remains stable while BF–BOF costs steadily increase. This shrinking cost gap, especially under the Net Zero scenario, highlights that more ambitious carbon pricing is crucial for improving the cost-competitiveness of EAF steel.

In 2032, the cost of abating one tonne of CO2 through the adoption of green H₂-Iron–EAF using grid electricity and without policy support is projected at USD 73–223/tCO2 under the BAU scenario and the Policy Enhancement scenario, and USD 21–171/tCO2 under the Net Zero scenario. Policy support can reduce these costs by a further USD 43/tCO2. These levels are markedly lower than the ratio of annual revenues to annual CO2 emissions for some domestic BF steelmakers (USD 415/tCO₂ for Nippon Steel and USD 492/tCO2 for JFE).42 43 44 45 This suggests that investment in green H₂-Iron–EAF offers both a substantial reduction in the financed emissions for domestic BF steelmakers and a pathway to economic viability. Stronger carbon pricing would reinforce this advantage, enabling steelmakers to deliver green steel at lower abatement costs.

Grid-based green H₂-HBI–EAF is the superior choice for decarbonisation compared to the LNG-based alternative. The LNG-based option is consistently over 4% more expensive. Furthermore, its emissions intensity is about 0.05 tCO2/tcs higher. While this difference is small, it is significant because it could push the steel’s emissions intensity past green steel thresholds, potentially making it unacceptable to buyers seeking truly low-carbon products.

Source: TA analysis, Superpower Institute37

Market Readiness and Price Premiums for Low-Carbon Steel in Japan

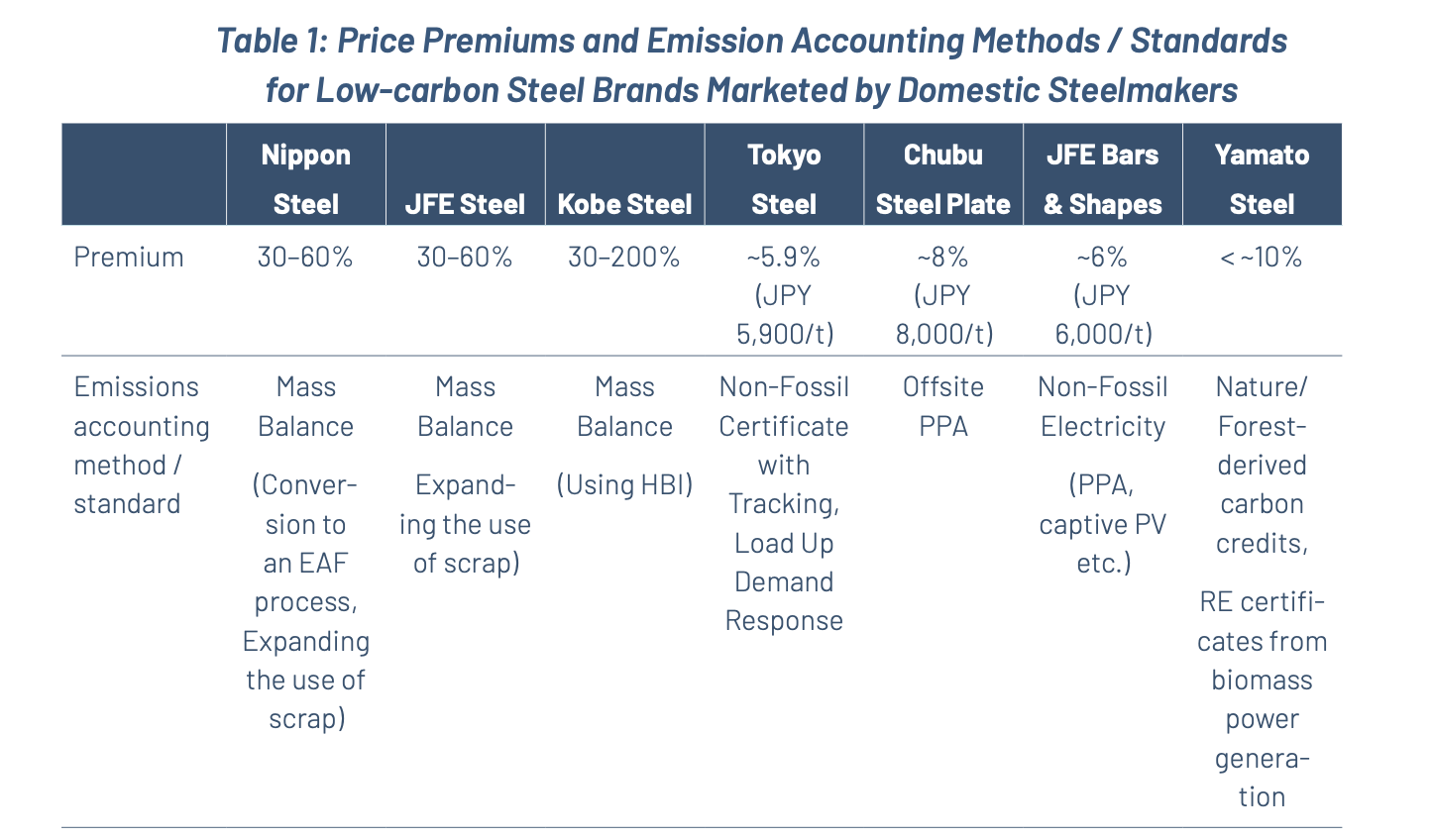

Several low-carbon steel products are already available in Japan. BF steelmakers apply the mass-balance approach and charge price premiums of over 30% (around JPY 30,000/t), while EAF steelmakers apply smaller premiums, typically under 10% (around JPY 10,000/t), for steel manufactured using RE. According to industry stakeholders, while domestic demand for these products, particularly steel produced using RE, is not yet substantial, there is nonetheless a certain level of interest. The main customers are said to be manufacturers and construction firms that are seeking to reduce their Scope 3 emissions.

By contrast, demand for mass-balance-based steel remains limited, partly because of doubts over whether such products can genuinely be considered “green”, and also due to its higher cost. In effect, Japan currently has very few low-carbon primary steel products whose environmental credentials are both reliable and aligned with customer expectations.

Moreover, as shown in Table 1, domestic EAF steelmakers already apply price premiums to low-carbon steel brands produced using RE. Assuming that green H2-Iron–EAF steel produced with RE could also be sold at a similar premium relative to grid-based production. Accordingly, when EAF steel is produced using RE procured through PPAs at current market rates (with green H2-HBI imported from the UAE) and sold at a price premium of JPY 5,900–10,000/t (~USD 39–67/t) above the cost of grid-based production, the resulting additional profit for steelmakers amounts to approximately 1% to 6% under various carbon pricing scenarios, which suggests that customers are still willing to pay the already high premium for green H₂-Iron–EAF steel.46

These results suggest that, under more stringent carbon pricing regimes, the production and sale of 100% RE-based green H2-Iron–EAF steel can offer steelmakers a potential profitability advantage on a per-tonne basis, as customers are still willing to pay the already high premium for it.

Sources: Company websites, news articles, interviews with industry stakeholders

Aligning Carbon Pricing, Energy Policy, and Industrial Strategy for Green Steel

Closing the cost gap between green H2-HBI–EAF steel and conventional BF–BOF production will require a coherent and integrated policy package that both strengthens investment incentives and supports demand for genuinely low-carbon steel. This analysis highlights several priority actions.

First, carbon pricing must be designed to drive genuine decarbonisation, rather than merely raising the cost of conventional steel.

Simply passing higher carbon costs on to BF–BOF producers risks accelerating the decline of domestic production without delivering commensurate emissions reductions. Ambitious benchmark settings, combined with an early and predictable reduction in free allocation under the GX-ETS, are therefore essential to redirect investment towards EAFs and other genuinely low-carbon technologies. Because the emissions advantages of green H2-HBI–EAF steel are intrinsic rather than accounting-based, this production route is also more likely to be recognised internationally as truly “green”, thereby supporting Japan’s competitiveness in export markets.

Second, policy support must address upstream cost reductions, particularly in green H2-HBI production.

Given Japan’s relatively high domestic RE costs, overseas H2-DRI production is likely to remain more economical, even after accounting for the additional costs of briquetting and long-distance transport. Preferential financing, such as concessional loans provided by institutions including JBIC, for investments in overseas green H2-HBI projects could therefore play an important role in reducing system-wide costs and securing long-term supply for Japanese steelmakers.

Third, achieving the full decarbonisation potential of EAFs is highly dependent on affordable access to renewable electricity – which must be driven by strong government support.

At present, renewable energy procurement in Japan is often not cost-competitive for most steelmakers, limiting both emissions reductions and the international credibility of domestically produced “green” steel.

This challenge reflects a combination of policy and market dynamics. Renewable electricity in Japan typically carries a price premium, and without clear demand-side incentives, EAF operators face the risk of locking into high-priced PPAs that may not be recoverable through product premiums. At the same time, government policy aims to deliver a power system that is both lower-cost and lower-carbon over the long term. In this context, many EAF operators may find it more rational to focus their efforts on advocating for faster grid decarbonisation and cost reductions, rather than committing capital to expensive PPAs today. While LNG-fired power generation can offer short-term emissions reductions, it does not represent a durable or economically robust pathway, particularly as carbon prices rise and grid emissions continue to decline.

As a result, sustained decarbonisation of the power sector remains critical. Until renewable electricity can be procured at scale and at competitive prices, falling grid emission factors will be the primary mechanism for reducing the carbon intensity of EAF steel production. Clear, credible power-sector decarbonisation targets, backed by concrete measures to accelerate the deployment of low-cost renewable capacity, will therefore be central to enabling meaningful and lasting emissions reductions in Japan’s steel sector.

Taken together, ambitious carbon pricing, upstream cost-reduction measures, expanded RE procurement options, and sustained grid decarbonisation can reinforce one another. An integrated approach of this kind would reduce investment risk, support stable demand for low-carbon steel, and provide a credible pathway for the long-term decarbonisation and international competitiveness of Japan’s steel industry.

Appendix 1: Scenarios’ Design and Assumptions

Source: TA analysis

Appendix 2: LCOS analysis

1.Levelized Cost of Steel (LCOS) Framework The economic feasibility of BF-BOF and green H2-Iron-EAF routes was evaluated using a bottom-up techno-economic assessment model. This model is grounded in rigorous mass and energy balances for each process route, derived from standard engineering parameters. The resulting Levelized Cost of Steel (LCOS) represents the breakeven price required to recover all capital and operational expenditures (CAPEX and OPEX) over the plant’s lifetime.

2.Regional Green H2-Iron Pricing Strategy To accurately reflect regional variances in feedstock costs, distinct sourcing strategies were applied for green iron:

- Australia (Pilbara, Geraldton, Kwinana): Green iron prices were sourced from the Superpower Institute, assuming inflexible production technology.

- Saudi Arabia & UAE: HBI prices were calculated using an in-house optimization model. This model determines the cost of Green H2-DRI by co-optimizing the capacity of electrolyzers, on-site renewable energy generation, and storage systems. It accounts for hourly operational profiles in hydrogen and HBI manufacturing. In the case of the UAE, the model additionally optimizes for grid electricity purchasing to supplement on-site generation.

3.Shipping cost: 10$/tDRI for shipping Green H2-Iron to Japan is counted

- 2025 Cost

- 2030 Cost Estimate:

a)The wind, solar, and li-ion storage CAPEX in SA and solar and li-ion storage CAPEX in AE are estimated using “best-in-class” benchmarks in 2025 as a conservative estimate of average 2030 price

b)The wind CAPEX in AE is estimated using 2025 global average, as AE wind is significantly higher than global average and there is limited data points on wind project in AE. By 2030, $1,041/kW would represent a significant (and plausible) reduction if the UAE moves toward larger utility-scale deployments.

c)Cost Estimate for Middle East from KAPSARC

d)Cost Estimate from US estimate * 90%

End Notes

- Green H2– Iron in this study includes both Hot Briquetted Iron (HBI) and Pig Iron

- https://www.worldbank.org/en/publication/state-and-trends-of-carbon-pricing

- https://www.env.go.jp/content/000209895.pdf

- https://icapcarbonaction.com/en/ets/eu-emissions-trading-system-eu-ets

- https://single-market-economy.ec.europa.eu/publications/european-steel-and-metals-action-plan_en

- https://www.jisf.or.jp/data/jyukyu/documents/jyukyu2505.pdf

- https://www.meti.go.jp/shingikai/mono_info_service/green_steel/pdf/003_06_00.pdf

- https://www.fudenkou.jp/fourum/docs/2025forum2.pdf

- https://www.enecho.meti.go.jp/en/category/special/article/detail_179.html

- https://www8.cao.go.jp/kisei-kaikaku/kisei/conference/energy/20231225/231225energy04.pdf

- https://www.meti.go.jp/shingikai/sankoshin/sangyo_gijutsu/emissions_trading/pdf/004_03_00.pdf

- https://www.meti.go.jp/shingikai/sankoshin/sangyo_gijutsu/emissions_trading/benchmark_wg/pdf/005_09_00.pdf

- https://www.cfp.energy/en/insights/the-eu-cbam-explained?utm_source=chatgpt.com

- https://www.renewable-ei.org/activities/column/reupdate/20250513.php#Reference

- https://www.nikkei.com/prime/gx/article/DGXZQOUC165WM0W5A011C2000000

- Projections for future carbon prices are assumed to increase linearly, based on the following sources: https://www.murc.jp/library/column/qmt_250620/; https://eneken.ieej.or.jp/data/11250.pdf ; https://iea.blob.core.windows.net/assets/86ede39e-4436-42d7-ba2a-edf61467e070/WorldEnergyOutlook2023.pdf

- Details of each scenario are provided in Appendix 1.

- https://pps-net.org/unit

- https://www.renewable-ei.org/pdfdownload/activities/REI_JPCorporatePPA_2025.pdf

- https://www.enecho.meti.go.jp/committee/council/basic_policy_subcommittee/mitoshi/cost_wg/2024/data/05_05.pdf

- https://www.enecho.meti.go.jp/category/others/basic_plan/pdf/20250218_02.pdf

- https://www.enecho.meti.go.jp/committee/council/basic_policy_subcommittee/2024/056/056_009.pdf

- https://www.nikkei.com/article/DGXZQOUC090CQ0Z00C25A4000000/

- https://www.enecho.meti.go.jp/committee/council/basic_policy_subcommittee/mitoshi/cost_wg/2024/data/01_07.pdf

- https://www.renewable-ei.org/pdfdownload/activities/REI_JPCorporatePPA_2025.pdf

- https://www.jpea.gr.jp/wp-content/uploads/sympo41_s4_doc2

- The Japan Iron and Steel Federation (JISF) has established the “Guidelines for Carbon Footprint Calculation of Non-Fossil Electricity Steel,” which state that non-fossil electricity steel should involve some form of investment or actual cost borne by the company. In other words, if RE is procured without incurring any extra cost, it does not qualify as non-fossil electricity steel under these guidelines. Furthermore, the Act on Promoting Green Procurement, which governs public procurement, calls on public bodies to give preference to products that contain steel complying with the JISF guidelines. Taken together, this suggests that RE procured without additional cost would not be recognised as non-fossil electricity under the guidelines, and that steel produced using such electricity would therefore be unlikely to qualify for preferential treatment in public procurement. https://www.jisf.or.jp/business/ondanka/kouken/greensteel/documents/Non-FossilPoweredSteelGuidelinev1.1.pdfhttps://public-comment.e-gov.go.jp/pcm/download?seqNo=0000302037

- https://transitionasia.org/voices-from-the-sector-japans-scrap-eaf-mills/

- https://cleanenergyconnect.jp/news/1235/

- https://www.renewable-ei.org/pdfdownload/activities/REI_JPCorporatePPA_2025.pdf

- The HBI values assume imports from Saudi Arabia

- https://www.nipponsteel.com/common/secure/works/kyushu/news/2025/pdf/20250411_100_09.pdf

- https://www.nikkei.com/article/DGXZQOJC02A7F0S5A700C2000000/

- https://e-lcs.jp/news/2024/10/2023co2.html

- Power generation costs for LNG (dedicated and hydrogen co-firing) and for 100% hydrogen firing are based on LCOE values published by Japan’s Agency for Natural Resources and Energy.https://www.enecho.meti.go.jp/committee/council/basic_policy_subcommittee/index.html#cost_wg

- https://www.superpowerinstitute.com.au/work/green-iron-plan

- https://www.meti.go.jp/shingikai/energy_environment/gx_carbon_footprint/pdf/001_04_00.pdf

- https://www.meti.go.jp/policy/economy/kyosoryoku_kyoka/senryaku_zeisei.html

- https://hta-process.jp/assets/pdf/kouboyouryou1008_ch1.pdf

- https://www.jfe-steel.co.jp/release/2024/12/241220-4.html

- https://www.nipponsteel.com/common/secure/news/20250530_200.pdf

- https://www.nipponsteel.com/en/ir/library/pdf/20250509_200.pdf

- https://www.nipponsteel.com/en/ir/library/pdf/nsc_en_ir_2025_databook.pdf

- https://azcms.ir-service.net/DATA/5411/ir/140120250507532922.pdf

- https://www.jfe-holdings.co.jp/en/common/pdf/sustainability/data/2025/sustainability2025e_A3.pdf

- Profit was calculated by deducting the cost from the assumed sales price

Data and Disclaimer

This analysis is for informational purposes only and does not constitute investment advice, and should not be relied upon to make any investment decision. The briefing represents the authors’ views and interpretations of publicly available information that is self-reported by the companies assessed. References are provided for company reporting but the authors did not seek to validate the public self-reported information provided by those companies. Therefore, the authors cannot guarantee the factual accuracy of all information presented in this briefing. The authors and Transition Asia expressly assume no liability for information used or published by third parties with reference to this report.

")